There’s lots to do when businesses engage a new worker. As an employer, you’ll be busy going through the onboarding process and showing your new employee the ropes, but there are other important things to do when you add a new member to your team.

Keeping accurate records complete with the right information is essential for businesses to maintain, and that means updating and adding data when engaging a new worker. Here are some things to keep in mind as you go through this process:

Every time you pay your worker, you might need to withhold a portion of their pay – called pay as you go (PAYG) withholding. This means that you hold on to some of your employee’s pay until tax time, which helps them to meet their end-of-year tax liabilities.

If you have other employees, you’re probably used to doing this, but when you engage a new worker it’s important to make sure you set all this up in your accounting software so you withhold the correct amounts and are meeting your reporting obligations. Do you need to up-skill using Xero, MYOB or QuickBooks for Payroll?

Here are a few more things you’ll need to find out to make sure your PAYG withholding for your new employee is up to par:

You’ll need to collect PAYG withholding amounts

The amount you need to withhold from your employee’s pay will depend on their individual circumstances. The rates are different for working holiday makers and workers hired under the Seasonal Worker Programme or Pacific Labour Scheme.

The ATO may also, in specific circumstances, issue a PAYG variation notice, in which case you’ll follow their varied amount given to you.

You can use the ATO’s tax withheld calculators to help figure out how much you need to collect, but you’ll need to get some information from your employee first, such as:

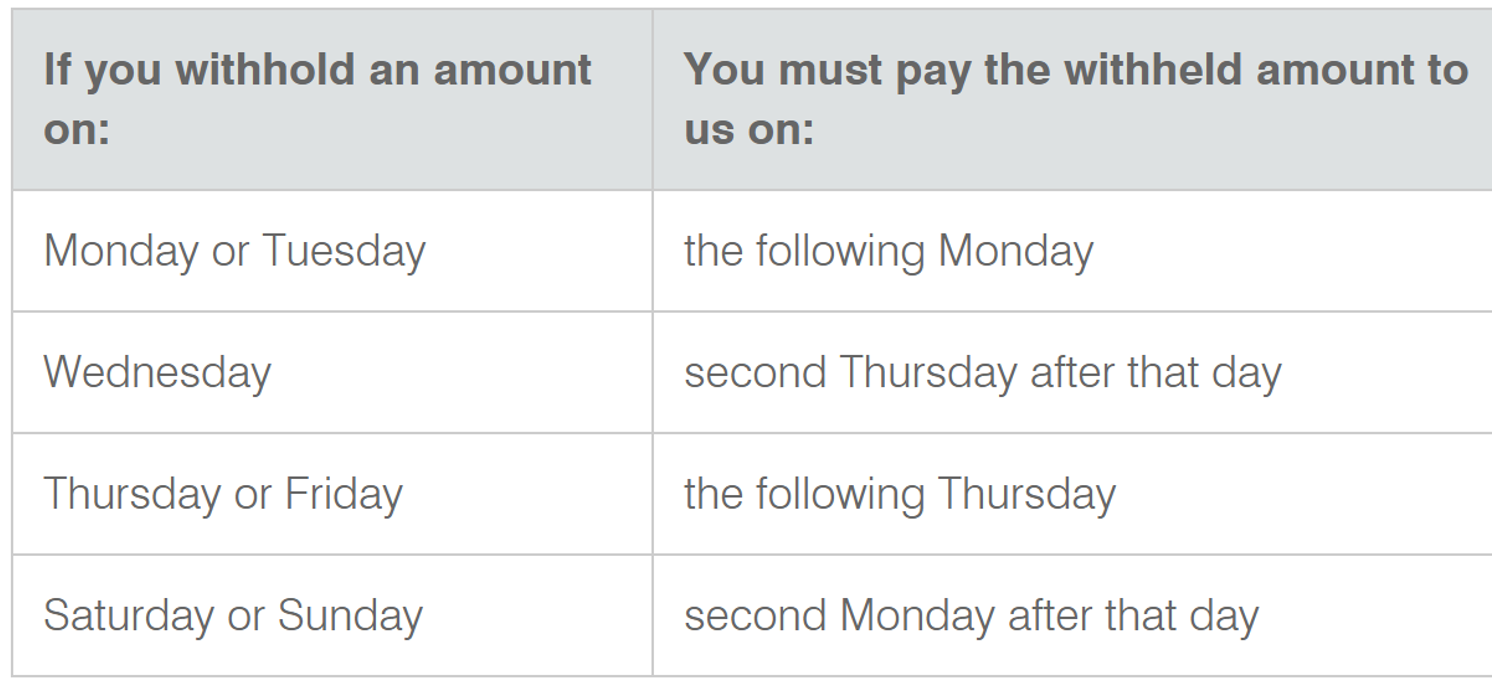

There are three categories of withholder: small, medium, and large. Whichever one your business is will impact how often you need to pay and report withheld amounts to the ATO.

Super guarantee (SG) is a contribution employers make towards their employee’s superannuation fund. It’s an important thing to stay on top of, especially considering the super guarantee charge (SGC) that applies if you fail to pay SG correctly.

We’ve written about SGC before, so you can find out how it impacts small businesses and how to avoid it!

Since the ATO scrapped the SG threshold, employees are eligible for SG contributions regardless of their income. So it’s highly likely your employee will be entitled to SG contributions form your business, meaning you’ll have to know when, where, and how much you need to contribute.

The SG rate is currently 10% of an employee’s earnings, but this rate will incrementally increase over time:

You also need to make sure you pay SG to the correct super fund of your employee by the correct date.

You can use a clearing house to have SG distributed on your behalf, but keep in mind that the payment will only be considered ‘paid’ on the date it’s received by the super fund, not the clearing house.

SG needs to be paid at a minimum quarterly, but you can pay more frequently if you want, as long as you pay your total quarterly obligation by the due date.

The ATO legally cannot extend the SG due date, so an important part of the onboarding process for a new employee is to get their super details into the system promptly.

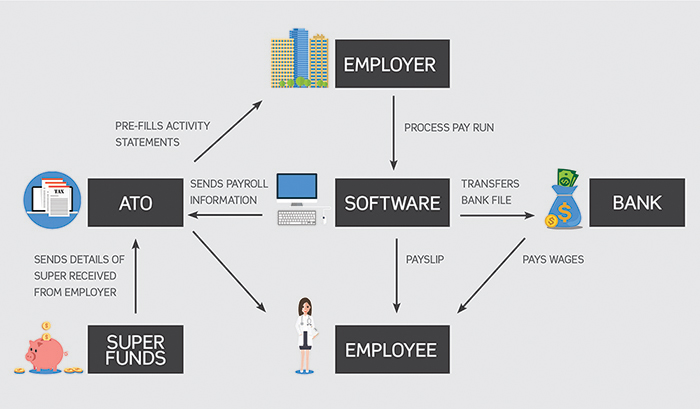

If this seems like a lot of information to keep track of, Single Touch Payroll (STP) makes the process a bit more streamlined.

STP means that as you run your payroll, you send a report to the ATO including important information such as salaries and wages, amounts withheld, and super liability information.

STP-enabled software, like MYOB AccountRight, MYOB Essentials, and Xero, sends a report with this information to the ATO. You’ll still need to finalise your STP at the end of the financial year, so that your employees can have access to their information in order to complete their tax return.

With the ATO announcing the roll out of STP Phase 2, it’s important to keep up to date with your employee information and reporting requirements. EzyLearn has already updated our payroll courses to cover STP Phase 2.

If you provide certain benefits to an employee, like covering the cost of their gym membership or providing free tickets to an event, this is called a fringe benefit. It’s different to salary or wages, and therefore has a different tax requirement called fringe benefit tax (FBT).

FBT is paid by an employer on the fringe benefits provided to employees, or employees’ families or other associates. It is calculated differently to income tax, instead being calculated on the taxable value of the fringe benefit.

As an employer, you have to self-assess your FBT liability and lodge an FBT return by 21 May (if you use a tax agent this date may differ). You can generally claim a tax deduction on the cost of the fringe benefits and the FBT paid, as well as claiming GST credits on fringe benefits items.

So if you’re bringing on a new worker and giving them personal use of a company car, or reimbursing them for school fees, make sure to keep record of it and consider how it will impact your FBT.

If you provide an employee over $2000 worth of certain fringe benefits in an FBT year (1 April – 31 March), then their grossed-up taxable value needs to be reported on their payment summary or through STP.

Jobs in Payroll Administration are in high demand because it requires more technical skill than other bookkeeping and accounts jobs. Learn more about the tasks performed by a Payroll Officer.

If you perform payroll administration services as a contract bookkeeper you’ll need to have a Cert IV in Accounting and Bookkeeping as a minimum starting point because Payroll tasks are considered a BAS Service by the ATO.

The most important thing in all of these points is keeping accurate records and staying on top of reporting obligations. To summarise, the key areas are:

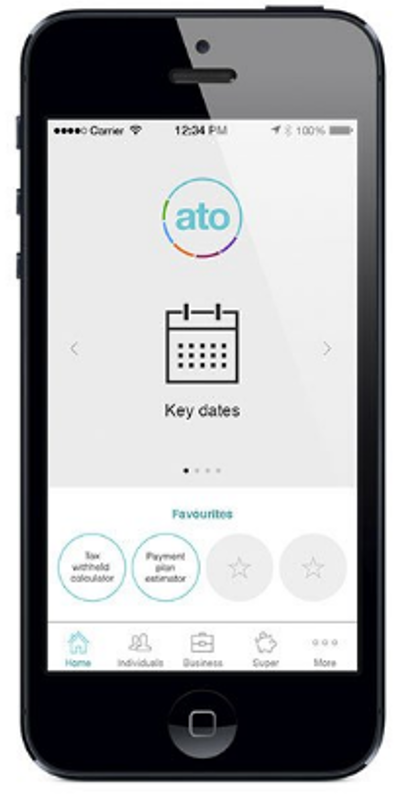

You can use the ATO mobile app to see when lodgements and payments are due, and in the instance of not being able to report/pay on time, you can contact the ATO to see what alternatives are available.

Using software like Xero, MYOB, and QuickBooks can help you to stay compliant with reporting obligations and keep accurate records.

Learn everything you need to know about payroll in one course with our NEW Advanced Certificate in Payroll Administration Combination Training Course Package, which includes all of our payroll courses across multiple accounting software.

Xero has always used its partner network to reach it's users. I remember one claim…

The purpose of a well designed course is to provide a series of steps for…

I've tried and tested hundreds of software programs over the last 25 years and I've…

Working with our graduates we've discovered that organisations are still looking for staff who can…

We receive lots of bookkeeping course enquiries from students who are changing careers and want…

Am I speaking gibberish or just crazy? No, I'm speaking the language of eInvoicing! PEPPOL…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}