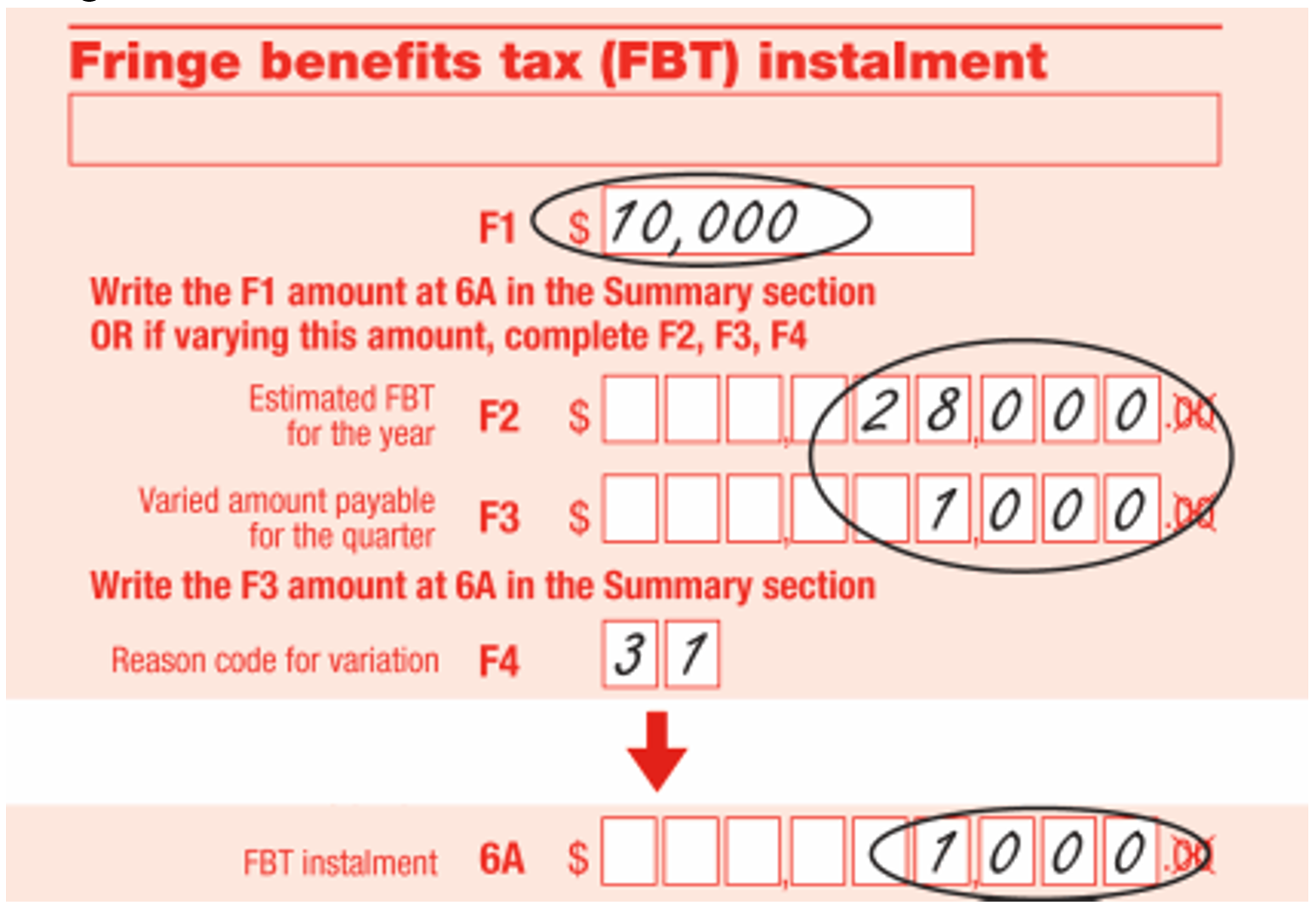

Do you provide your employees with gym memberships or concert tickets? Or maybe you work for a company that provides you with a vehicle or accommodation? There are lots of perks that business can provide to their employees outside of salaries and wages – and these are called fringe benefits and they may apply to you if you worked at home due to COVID-19.

FBT is not as simple as handing out freebies. Employers have to pay tax on these benefits they provide, and the amount can depend on the type of fringe benefit they’re providing.

We’ve written before about how fringe benefits tax is important to consider when you engage a new worker, but let’s look more in-depth into what fringe benefits are all about, and how to ensure you comply with your liabilities:

Repayments on a business loan may be less than super and PAYG combined

It’s not uncommon for small businesses to take out a business loan to meet their super and PAYG obligations – but this should never be a knee-jerk reaction to lean times.

Depending on how many employees work for you, the repayments on a business loan are typically smaller than all of your payroll obligations — this includes superannuation and PAYG — combined. If you get a loan to fund 12 months of your business, payable over a 24 or 26 month period, the repayments will be far easier to manage each month.

Interest is usually a tax deduction

Businesses are able to claim the interest from any business loan as a tax deduction, so even if the annual percentage rate (APR) adds a few additional thousands of dollars to your capital amount over the period it takes to pay the loan back, the interest will still go towards reducing your taxable income.

This is a more favourable option to delaying payment to your employees (illegal) and delaying payment of PAYG and superannuation withholdings, which could incur a Failure To Lodge (FTL) penalty, plus a general interest charge (GIC). Note: Fines and penalties cannot be claimed as a tax deduction and are therefore dead money.

Do your sums first

Don’t forget that, while a business loan to cover payroll for 12 months will be easy to repay initially, your business’s profits will need to improve substantially over the next year so that you can continue to meet your loan repayments AND your payroll obligations for that year.

***

You can easily work this out using Microsoft Excel. Our Intermediate Microsoft Excel training courses show you how to determine if you can afford to take out a mortgage, but because all of our fields remain “unlocked”, you can easily modify them to suit a business loan scenario. Visit our website for more information on all of our Excel training courses.

Our online training courses feature real-life case studies to make our learning more relevant and true to life.

Using Excel to work out your PAYG and super obligations is a great way for small businesses, with a small number of employees, to save money. It saves you having to purchase this extra module in MYOB or Xero, for instance, when you may rarely use it. Saving money for small business is crucial as often it’s these same small businesses that have trouble making payroll payments each week, fortnight or month — and then wind up incurring further fees from the ATO when they’re late with their reporting and payments. It’s a vicious cycle.

Get financing. There are lots of ways to do this, but a common method, particularly if you need access to funds quickly, is to get a short-term business loan. Many short-term business loans don’t require businesses to have a great credit score, and will offer funding of as little as $5,000 right up to $500,000.

You’d have between 3 and 36 months to pay back the loan, but you need to be aware — the annual percentage rates (APR) are usually high. Most lenders require the business to have been active for a minimum of 9 months, and have revenue of more than $75,000 per annum. However, if paid off quickly, these can be an alternative to incurring penalties — it will obviously depend on your business’ individual circumstances.

Keep on top of bookkeeping

If you stay on top of your bookkeeping, you’ll either reduce the likelihood that you won’t make payroll, or as a worst case scenario, be able to foresee the periods when you won’t be able to, and be able to arrange finance in time to cover it.

***

Use the Ad Hoc Payroll Guide included in our Intermediate Microsoft Excel training courses to determine the rate of PAYG tax to withhold — and the required super contribution amounts in Excel. Visit our website for more information on our entire suite of Excel training courses.

Don’t get lumped with penalties when you don’t need to!

It’s not only frustrating and disheartening, but a waste of business funds to be penalised for lodging your financials too late.

A LOT OF SMALL BUSINESSES have trouble managing their payroll, especially when they only have a few employees and paying to access a payroll system in their accounting package is an unnecessary expense. You’ll learn how to use Excel to manage your PAYG and super contributions in our Intermediate Microsoft Excel Training Courses. However, sometimes you may have a backlog of PAYG and super payments. Let’s take a look at how to manage these.

For businesses that only withhold up to $25,000 each year, you’re supposed to make PAYG payments and file a withholding report each quarter. You have 28 days from the end of the quarter to do so, after which time, you may incur a Failure To Lodge (FTL) penalty.

Superannuation payments

As with PAYG payments and reporting, you can also incur a FTL penalty for not lodging or paying your employees’ superannuation contributions in time. All businesses, regardless of size, have to make superannuation payments each quarter — the ATO sets out the due dates for each period on their website.

Lodging late PAYG and super payments

The ATO only applies penalties for failure to lodge reports or make payments for each period of 28 days (or part thereof) that a document or payment is overdue. Each period incurs one penalty unit for each document, up to a maximum of five penalty units.

From 2015 onwards, the value of a penalty unit is $180 (previously it was $170) for small businesses, which are defined as entities with an assessable income or GST turnover of no more than $1 million a year.

The maximum penalty a small business will pay is $900 for each document or payment that is overdue. Note too that FTL penalties will also incur a general interest charge (GIC), applied on top of the penalty.

Managing late PAYG and super payments

Use the Ad Hoc Payroll Guide, a new case study that is included in our Intermediate Microsoft Excel Training Coursesto determine the rate of PAYG tax to withhold and the required super contribution amounts in Excel. Once you’ve worked out the required amounts (visit the ATO website for tax tables prior to 2017), lodge the necessary PAYG payments and reports to the ATO; pay super contributions using the SuperStream super clearing house.

The ATO will write to you if you are required to pay a penalty — sometimes they are waived for first-time offences, or if the amounts are small.

Create brilliant presentations and graphics for all kinds of business purposes.

Gone are the days of excruciatingly dull PowerPoint slide presentations. Nowadays PowerPoint is the hidden gem used to generate animations, videos, movies, advertising and graphics. It’s a great ally to the marketer or social media person in your organisation.

This creative program can also be used to conjure up the most beautiful and modern pictorial slides to enhance any presentation or induction. Find out more about our 2016 version PowerPoint courses.

Third Quarter is Looming; Are You Up to Date with Payroll?

Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.

Every Australian business with employees who are each paid more than the tax-free threshold has a legal obligation to withhold tax on their employees’ behalf. This is known as the PAYG System (or Pay As You Go), where amounts of tax are withheld from each employee’s wage payments.

Businesses that withhold up to $25,000 each year only need to make payments to the ATO each quarter; businesses withholding amounts greater than $25,001 may have to make payments to the ATO each month or as regularly as each week.

At the time of writing, the tax-free threshold is currently $18,200, which is equivalent to:

$350 a week

$700 a fortnight

$1,517 a month

Superannuation contributions

Again, any business that pays its employees more than $450 each month must also make regular superannuation contributions on their employees’ behalf. We’ve written in the past about the government’s clearing house called SuperStream, which allows you to easily make super contributions — for free.

But first, you need to work out how much super you need to contribute for your employees. The superannuation guarantee is currently 9.5 percent of your employees’ gross wages, which is payable on top of their wages — not deducted out of.

Using tax tables to calculate wages

Each year, the ATO produces a range of tax tables to help you work out how much to withhold from payments you make to your employees. In our Ad Hoc Payroll Micro Course, we’ve already added the most current tax tables to the accompanying payroll spreadsheet, as well as the superannuation guarantee tables.

We recently witness a federal budget and there are usually some changes in each budget that relate to tax tables or tax thresholds. These tax tables simply define how much tax you pay for each threshold and the simplest way to describe it is to define the first category. This category is called the tax-free threshold and it is the level at which you don’t pay any tax. The annual pay for this level will be $18,200 from 1st July 2012 (the beginning of the next financial year). Any money you earn up to this level you don’t pay any income tax on.

Any money you earn over this tax-free threshold amount but less than $37,000 will be taxed at 19c per dollar.

The most important thing to note is that just because you earn $50,000 doesn’t mean you will be taxed at 32.5c in every dollar you earn. You’ll be charged

zero for the first $18,200,

19% from $18,200 to $37,000 and then

32.50% for each dollar over $37,000.

Stay tuned for more bite size chunks of knowledge in the coming weeks as we evolve our MYOB Payroll training course. Make sure you subscribe to receive these posts via email.

Search this site

Type the first 3 characters to discover courses, up-skilling programs and CPD articles.

EzyLearn's Career Academy

Enrolled into an EzyLearn course since 2013? Get access to new & updated course content and support by joining the EzyLearn Course Refresher Access membership Program. See how to extend your course life & support.

Xero is a great bookkeeping program for tradies who are on the go and using their phones (or a tablet) all the time. From receipts scanning to creating quotes and invoices, receiving payments and keeping track of project costs.

bookkeepercourse.com.au/produ…

Don’t forget that, while a business loan to cover payroll for 12 months will be easy to repay initially, your business’s profits will need to improve substantially over the next year so that you can continue to meet your loan repayments AND your payroll obligations for that year.

Don’t forget that, while a business loan to cover payroll for 12 months will be easy to repay initially, your business’s profits will need to improve substantially over the next year so that you can continue to meet your loan repayments AND your payroll obligations for that year.

EzyLearn Excel, MYOB and Xero online training courses count towards

EzyLearn Excel, MYOB and Xero online training courses count towards  Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.

Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.