Reconciling Your Accounts Daily Gives a True Picture of Cash Flow

The king was in his counting house, counting out his money… small businesses as well as large can get a true financial picture with daily reconciliation.

For a lot of business owners, just the thought of reconciling their accounts once a month is enough to make them go weak at the knees, never mind every day.

Some business owners feel that bank reconciliation is wasted time that doesn’t bring in revenue, yet there are plenty of contract and remote bookkeepers who work for their clients each week, and some that work every day for the same client, reconciling their accounts and providing other vital bookkeeping services.

And they’re not just big businesses whose accounts are reconciled daily — plenty of small businesses do so too.

In fact, with so many small businesses going asunder due to cash flow problems (often stemming from a lack of procedures in place for credit and debt management) it can be not only a cost-saver but a potential life-saver to your business.

If using online reviews to help you work out what to buy, you want to make sure you’re really hearing it from the horse’s mouth, and not just reading fake marketing guff.

IF YOU’RE ANYTHING LIKE most people, rating and reviews are how you probably make many of your purchase decisions. This can be for purchasing white goods, clothing, a holiday, or even choosing a real estate agent.Continue reading Can You Trust Online Ratings and Reviews?

A bookkeeper who’s certified in a particular accounting software may not mean that much for your business. Better to have someone who is simply a good bookkeeper. Period.

Now that virtual bookkeepers have become more common, lots of business owners have started selecting bookkeepers based on their affiliation with an accounting application. Such bookkeepers are often called a Certified Advisor (Xero), Pro Advisor (QuickBooks) or Certified Consultant (MYOB). But are they really the best bookkeeper for your business?

What are Certified Advisors, Consultants and Pro Advisors?

In a nutshell, a certified advisor, consultant or pro advisor is just an individual who has been endorsed by a software company because they’ve demonstrated a high level of knowledge and skill with a particular accounting product.

Hiring a bookkeeper who’s been endorsed by MYOB, say, means you shouldn’t have to worry about whether your bookkeeper has set up your accounting package correctly, or whether they’re using the correct codes. What it doesn’t guarantee, however, is that each consultant or advisor is a highly experienced BAS agent, as the certification relates to their software knowledge only.

Certified Advisors and Pro Advisors go through their certificate, which is often free, because it elevates their own profile. It can also demonstrate that they are committed to that software program more than others. The Xero Certification training (at the time of writing) has a strong focus on understanding how to use the Xero Agent portal to bring clients onto the platform – and not so much about learning bookkeeping or to become a BAS Agent.

If you don’t have an accountant or BAS Agent then you should make that your starting point as everyone needs someone who can perform tasks that relate to tax and GST who acts on your behalf. If you have that setup already you can hire someone who has good bookkeeping skills using MYOB or Xero but is cheaper because they are not registered or licensed. This junior bookkeeper can perform your office admin, accounts and even customer service while your Registered BAS Agent or Tax Accountant can sign off on your financial figures.

Find a highly qualified BAS or tax agent instead

Sure, a bookkeeper who’s experienced in your accounting package is important. It’ll help keep your bookkeeping bill down because they’re able to perform certain functions quickly, while your accountant shouldn’t need to fix any errors, either. But that’s only providing that they’re as knowledgeable in Australian tax as they are MYOB or Xero or QuickBooks.

Unfortunately, however, the two aren’t mutually exclusive. So instead of focussing on a bookkeeper’s software experience, it’s more beneficial to ensure they’re qualified BAS and tax agents, with either a Certificate IV in Bookkeeping or higher.

If you don’t get a bad reference from their current and former clients, then there’s a pretty good chance they’re proficient in the major accounting packages, and if they’re not, most bookkeepers will tell you upfront.

Get the accounting package that’s best for your business, not your bookkeeper

There are lots of reasons a bookkeeper would choose to become certified with a software company, the biggest being that they get their accounting software for free and receive a commission for each new client they sign up to use the accounting package they’ve been certified with.

However, when you hire an independent bookkeeper who’s well-versed in a few different accounting packages, you’re more likely to get better advice about which accounting package is best suited to you and your business’s needs, rather than the accounting package that will generate income for your bookkeeper.

***

Are you looking to brush up your skills in cloud-accounting packages like XERO, MYOB or Quickbooks? We provide a range of online training courses in all of these packages at ONE LOW COST for ALL SKILLS LEVELS. Find out more.

We feature our own online directory of local bookkeepers looking to add to their customers. Visit National Bookkeeping to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

Excel isn’t just for budding bookkeepers; it’s a great tool for all business owners to know.

MICROSOFT EXCEL IS THE most widely used spreadsheet application in modern computing. That said, it’s also one of the more difficult programs of the Microsoft Office Suite to learn, which is why we recently updated the content of our Excel training courses.

A lot of people do our Excel training courses to help them “skill up” to find a job, find a position better suited to them, or develop their career path. However, Excel is a fantastic tool for small business owners as well.

But whether you use Excel to create a pivot table or a database, there are a few things you should do each time you open an Excel document. Here we present you with three:

1. Vertical align: always centre

Always align the text in the cells of your Excel spreadsheet to the centre, or the top in certain circumstances. But never, ever align it to the bottom. It’s hard on the eyes and, when you’re looking at lots and lots of data in lots and lots of cells, it becomes difficult to know which row, column, etc, you’re looking in. Centre alignment, always.

2. Build error-checking into formulas

There should never be an instance where one of your workbooks is showing a #DIV/0, #N/A, #REF, #NAME?, #NUM!, or #NULL! error. This is especially true if you’re sharing these workbooks with your business partners or accountant or whomever.

Seeing an error in a financial report may cause the reader to doubt the accuracy of the entire workbook, so ensure your workbooks remain error free by using the simple IFERROR() error-checking function in Excel.

3. Print preview your work

Again, if you intend to share workbooks with other people, you should always ensure that your Excel workbooks can be printed nicely and easily, even if you don’t intend to ever print the document yourself. This is easy enough to do via File > Print Preview and adjusting the print margins before sharing (or printing) the document.

However, judging by the number of times I’ve printed an Excel document only to collect 87 sheets of paper off my printer to read the contents one 4×4 table, the function is seldom used by anyone else but me!

***

For more Excel formatting tips and tricks, download our FREE Beginners’ Guide to Excel, or enrol in our intermediate or advanced online Excel training courses to learn how to create databases, pivot tables, charts, graphs, and much more…

This time we’re looking at other expense applications that not only integrate with Xero, but other platforms like MYOB and QuickBooks, too. (For the record, every transaction Expensify does with Xero, it also does with QuickBooks; and also for the record, we not only provide online training in Xero [all levels for one low cost] but MYOB and Quickbooks too.)

Here are some other expense tracking app integrations.

It can be easy to lose track of separate income streams; Excel is a great tool for monitoring which work your income is coming from.

IF YOU’RE AN INDEPENDENT contractor, or you’re a full-time employee about to start up a side business, then you need to be able to keep a good track of all your income streams. There are a couple of reasons for this and both of them relate to tax. Continue reading What to Do When You Have More than One Income Stream

The simple act of creating an Excel spreadsheet to itemise your expenses can help you keep track of everything eating into your business’ cashflow – even if not strictly deductible.

HAVE YOU RECENTLY STARTED running your own business? Whether you have, or whether you’re about to, reconciling your bank accounts regularly is probably one of the best ways to monitor your expenditure in relation to your income.

Your accounting software will help you to keep track of your income and business expenses and other important things that will affect your start up — such as how long it takes to get paid — while an Excel spending or expense sheet will help you to monitor all of your spending, business or otherwise.

The bank reconciliation process

This starts when you get your bank statement, but you can speed the process up, by entering recurring expenses into your Excel spreadsheet as they occur.

In your Excel spending sheet, you’ll enter the expense in total, but in your accounting software, you’ll only enter the percentage of the expense that relates to your business.

Identify cash flow problems

If your business has poor cash flow, using an Excel spending sheet in addition to your accounting software will allow you to identify what’s causing your cash flow problems. Sometimes cash flow problems are caused by later payers, due to poor credit management processes. Other times, however, you may find that you’re simply not earning enough to cover your expenses each week or month.

To remedy this immediately, you should look through your Excel spending sheet and see if there are any expenses, either business or discretionary ones, that you can reduce or eliminate. Then you should work on increasing your income. That’s easier said than done, which is why you should reduce your spending first.

Forecasting profit

If you don’t identify any cash flow issues, you will be able to begin forecasting profit. Typically, profit just refers to the income left over after all your business expenses have been accounted for.

But there are plenty of start ups and sole traders, who have a profitable business but are not profitable themselves.

That’s because there are many other expenses in your ordinary life — the remaining 70 percent of your internet bill, for example — that you still need to pay for.

If you’re also recording all your other expenses in an Excel spending sheet, you’ll be able to forecast your business’s profit, as well as your own personal profit (otherwise known as savings) with much greater accuracy.

The chart of accounts

In effect, what you’re doing here is creating a chart of accounts. You’ll learn more about the chart of accounts in our Xero and MYOB courses, but they are, in a nutshell, a financial record of every account — asset, liability, equity, revenue, etc — in your business.

Why Excel is Great for Keeping Track of Your Spending if You’re Self Employed

That take away coffee that you buy each morning should be added to your business expenses sheet; even if not claimable it shows where your money is going.

WHETHER YOU’RE ABOUT TO start your own bookkeeping business, or whether you work as an independent contractor (even if you’ve been doing this for a while), it’s really important to know how much you’re spending each month.

Your Xero, MYOB or QuickBooks accounting software will help you with some of this, but the very best way is to create an expense or spending sheet in Excel — which we teach you how to do in our Excel training courses — as this gives you a far more detailed look at your expenses and spending.

Not all your expenses are 100% business ones

Sometimes you can’t claim 100 percent of your expenses as business ones — the costs of running your car, home internet, rent, utilities, etc — but you should nevertheless keep track of your spending on these items because it will affect your cash flow.

That’s why keeping an Excel spending or expense sheet is a good idea for contractors and home-based business owners. You don’t want to enter your home internet into your accounting software as a business expense, if only 30 percent of it is used for business purposes, but you still need to keep track of it, so you can manage your cashflow.

Monitor frivolous spending

One of the things we love about using Excel to track your expenses and spending is that every little expenditure is right there, in plain view.

This isn’t the case with Xero or MYOB or other accounting software. Your expenses are hidden away, and you have to run a report to get a good breakdown on where your money is going.

Not so with Excel,. If you buy a coffee every morning, it’s right there, in a category you can label as “coffee”.

Now, we’re not saying that coffee is frivolous. Far from it. Many of us need coffee just to function (!) but there are lots of small things we spend money on every day, week, month that add up. When you’re self-employed you need to keep an eye on these “little” things.

Sometimes, you’ll find that you’re spending lots of money each month on subscription services that you’re not even using. Eliminating $15 a month here and there makes a big difference.

Create as many categories as you need

That’s the other great thing about using Excel to track your spending: You can create all the expense categories you like.

Of course, not everyone wants to track each and every expense right down to their last bag of jelly beans — that actually would be a little ridiculous — and for most the most part, you can lump your groceries into a category for discretionary spending, but there are some things you might want to separate out — movie tickets, money spent on lunches and dinners, and so forth.

These things tend to add up, and if you want to keep an eye on them, separating them out is the easiest way to do that.

Back to those business expenses

Each fortnight or month or however regularly you complete your bookkeeping, you can easily add in those business expenses into your accounting software — or your bookkeeper can.

Remember, if you spend $60 a month on internet, but only 30 percent of its use is for business purposes, you should only add $18 a month as a business expense in your accounting software. In your Excel expense or spending sheet, however, you’ll put the full $60 in, as you need to have the money in the bank to cover this expense each month.

***

You can learn how to create and manage your expenses or spending in our Excel training courses, where you’ll be able to create your own spending or expense sheet. Visit our website for more information.

Dive deep into your claimable expenses and don’t forget all those smaller prepaid expenses like magazine subscriptions or domain name registrations – you can only claim all of these during the period in which they occurred.

WE’RE IN THE LAST QUARTER of the 2016/17 financial year, so now is the time to dive in deep and check you’ve included every single business expense — prepaid or otherwise — to ensure all your expenses are in order.

We all know this, but remember, they can only be claimed for the period in which they occurred. If you forget to claim a major business expense in the financial year that it occurred, you can’t make it up by claiming it the next year.

It’s really important you thoroughly check your credit cards and business accounts to make sure you’ve accounted for each expense. The final quarter of the financial year is also a good time to make any purchases for your business, because you can claim them straight away.

Prepaid expenses are often forgotten

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

These deductions are often prepaid and may not come up on your radar and may certainly not show up on your final quarter bank statements.

Make a list and check it twice

Over the next month or so, make a list of all of your expenses as you think of them. This makes it easy to spot them when you’re going through your bank and credit card statements and checking them against the expenses in your accounting software.

Want to make your business presentations and publications more eye catching?

Gone are the days of excruciatingly dull PowerPoint slide presentations. Nowadays PowerPoint is the hidden gem used to generate animations, videos, movies, advertising and graphics. It’s a great ally to the marketer or social media person in your organisation.

Depending on the structure of your business, you may be legally required to include a P&L statement with your tax return or activity statements. Your tax agent will be able to advise you if your business will be required to file a P&L, which requires all of your bookkeeping to be up-to-date before you can run it.

Even if you don’t have to file one with your activity statements or tax returns, it’s still a good idea to run a P&L for your own sake. A P&L statement identifies whether your business has made a profit or loss and which accounting period these occurred.

Accounts receivable, payable

Find out who owes money to your business and to whom your business owes money. This is obviously part of the credit management process, which any good business will have in place already, but it’s a good idea to keep a steady eye on what’s coming in and what’s going out as EOFY approaches.

PAYG, superannuation

The end of each quarter brings a lot of PAYG and superannuation reporting, but EOFY brings a double whammy of activity statements tax returns and PAYG and superannuation compliance. You’ll need to run these reports so your bookkeeper can complete the payroll component of your returns.

Inventory stocktake

If you sell goods, you’ll need to complete a stocktake of your business’s inventory so that any missing stock can be written off, and to ensure you’re starting a clean slate for the new financial year.

WE’VE ENTERED QUARTER 4 for the 2016/17 financial year, so we’ve been writing about the things your business should be doing this quarter in preparation for the end of the financial year. In our last post we wrote about writing off stock and inventory. Now we’re looking at business expenses.

We show you how to write off stock and inventory before the EOFY

Do you know how to make inventory adjustments? Our Xero and MYOB BAS and GST Reporting courses can show you how.

IT’S A GOOD TIME TO START looking at any slow-moving or obsolete stock that your business (or your client’s business) may be holding, as we’ve reached the end of Quarter 3 and have now started Quarter 4 for the 2016/17 financial year — which means the end of the financial year is fast approaching.

Writing off stock in MYOB or Xero is known as making an inventory adjustment, and our MYOB BAS Reporting and GST or Xero GST, Reporting and BAS training courses take you through the steps to do this. But first, you need to identify which items aren’t selling. We’ve created this case study to help you understand how.

Understanding your inventory’s performance

Every business needs to understand how their inventory is performing, and how it impacts their business. If the business owner is too busy to stay on top of this, then they should employ a bookkeeper to help.

A good example of why understanding inventory is important to a business is to look at an air conditioning company. This business makes money two ways:

Selling air conditioning units

Installing / maintaining air conditioning units

The margin on the sale of an air conditioning unit is not much, a few percent on top of the wholesale price. Where the business makes its money is in the installation or maintenance of the units it sells.

The business purchases three dozen units, of varying brands, models, price points, etcetera. It now needs to know which units are most popular with customers and why; which units aren’t popular with customers and why; whether it’s profitable for the business to continue to stock the unpopular units; or, conversely, whether it’s profitable for the business to continue stocking the popular units.

Inventory reporting

The business’s bookkeeper regularly runs a number of reports in their accounting software, including profit and loss reports and stock-on-hand reports. These reports are used to identify which units sell quickly, as well as the units that take longer to sell, and the profit margins on each.

The units that sell quickly don’t require a technician to install them. Although they’re responsible for the majority of sales, they don’t generate more revenue for the business. The units that sell slowly, do generate more revenue as they require installation and maintenance, however too many units were ordered and they’ve now been discontinued by the manufacturer. Some units have hardly sold, and, although not discontinued, have been superseded by newer models.

Stock write offs and future orders

Because the bookkeeper regularly runs these reports, s/he has been able to export them into Excel for further analysis. By the end of Q3, the bookkeeper can make suggestions to the business owner about the future of the business.

In particular, the bookkeeper suggests that the units that have been superseded are marked down to clear as much stock as possible, and cease any new orders. Likewise, the discontinued models will be marked down.

Orders for the units that replaced the discontinued models will halve the order volume. Likewise, order volumes for the top selling units will reduced. The profit margin on these units is very low and they result in no additional revenue from installation or maintenance. The profit that would be earned on the additional units is negligible, however by reducing the unit volumes, the business improves its cash flow.

Act NOW for EOFY

If your business sells stock or a combination of stock and services, like the air conditioning business does above, start looking at your inventory now. Markdown any slow-moving stock at the end of Q3, to give your business time to move the remainder of it. If it doesn’t sell, write it off at EOFY.

We feature our own online directory of local bookkeepers looking to add to their customers. Visit National Bookkeeping to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

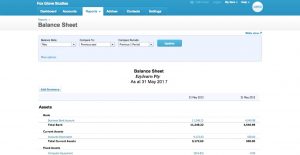

A business’s balance sheet is a snapshot of its financial position at a particular period of time, which is not to be confused with a profit and loss (P&L) statement. Unlike a P&L, which just shows whether the business is making a profit or loss during a given period, a balance sheet, will eventually, show nearly every activity that has occurred within a business.

However, there are some transactions that will show up immediately. You’ll learn how to run a balance sheet in our Xero Daily Reconciliations Training Course, but we wanted to show you the transactions to look out for and why.

A balance sheet reveals the nitty gritty of your business’ transactions.

The purchase or sale of assets

When an asset, such as a car, is bought, it will reduce the cash account and increase the fixed-assets account. Both of these accounts are listed in the asset portion of the balance sheet, however, cash is part of the current assets section and fixed assets are part of the long-term assets section.

When an asset is sold, the way the cash is accounted for is a bit more difficult. Here, both the asset’s book value and any accumulated depreciation are removed from the books at the same time that the cash account is increased by the sales price. If the sales price does not equal the book value, the difference is accounted for as a gain or loss on the sale of equipment. This gain or loss is recorded on the P&L statement.

Purchases on credit

When a business purchases supplies or inventory on credit, the business will debit the asset account (supplies or inventory) and credit the accounts-payable account. Almost always, accounts payable are considered to be current liabilities and are shown at the top of the liabilities section of the balance sheet.

Debt and lease arrangements

When a business issues debt or enters into a leasing arrangement, a liability must be recorded in the long-term section of the company’s balance sheet. For example, if a company issues bonds for cash, the company would debit cash and credit bonds payable in the simplest bond-issuance scenarios.

Capital-lease transactions affect the balance sheet in a similar manner. When entering a capital-lease arrangement, the business will debit a fixed-asset account to show that the company has taken economic possession of the leased asset. At the same time, the business will credit a capital-lease obligation account to show the offsetting economic liability.

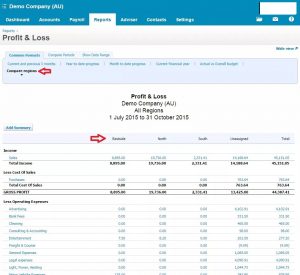

Profit and loss statements should be run by businesses regularly and are required by law.

A basic, yet vitally important, report for every business owner is a profit and loss (P&L) statement. A profit and loss statement, as the name suggests, shows whether a business is running at a profit or a loss over a given period. We’ve written about why running multi-period P&Ls before in QuickBooks and MYOB is a good idea for businesses with inventory, but single period P&Ls are equally important for all businesses.

If you’re a bookkeeping newbie, a profit and loss statement, which sometimes goes by other names — income statements, earning statements, revenue statements, operating statements, statement of operations, or statement of financial performance — is a basic report you’ll learn to run in our Xero Daily Reconciliations Course. If you’re planning to work as a contract bookkeeper, you should get in the habit of running P&L statements for your clients regularly (if you’re a business owner, ask your bookkeeper to run them).

P&Ls are required by law

Depending on how a business is structured, it may be required by law to complete a P&L. A P&L shows how the revenue of the business is turned into net income by subtracting all expenses from income. They’re also useful for understanding a business’ net income, which helps with the decision making processes. A business will also need a P&L if they’re applying for a small business loan.

The contents of a P&L

Although the process of running a P&L differ between accounting software packages, they usually all contain the same elements, depending only on the business itself. In the first section, the cost of sales is subtracted from the revenue, which highlights gross profit. The business’ operating expenses are then subtracted from the gross profit, which leaves the operating profit. Now, all of the non-operating revenues and expenses must be factored into account, after which the business’ profit or loss will be displayed.

***

Because P&L statements are often used by a business’ owner to make financial decisions, to inform shareholders of the business’ performance, apply for a business loan, or as proof of income in the sale of a business, it’s important that you understand how to create one correctly. Our Xero Daily Reconciliations Training Course covers P&L statements, and much more. Visit our website to learn more or to enrol.

Third Quarter is Looming; Are You Up to Date with Payroll?

Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.

Every Australian business with employees who are each paid more than the tax-free threshold has a legal obligation to withhold tax on their employees’ behalf. This is known as the PAYG System (or Pay As You Go), where amounts of tax are withheld from each employee’s wage payments.

Businesses that withhold up to $25,000 each year only need to make payments to the ATO each quarter; businesses withholding amounts greater than $25,001 may have to make payments to the ATO each month or as regularly as each week.

At the time of writing, the tax-free threshold is currently $18,200, which is equivalent to:

$350 a week

$700 a fortnight

$1,517 a month

Superannuation contributions

Again, any business that pays its employees more than $450 each month must also make regular superannuation contributions on their employees’ behalf. We’ve written in the past about the government’s clearing house called SuperStream, which allows you to easily make super contributions — for free.

But first, you need to work out how much super you need to contribute for your employees. The superannuation guarantee is currently 9.5 percent of your employees’ gross wages, which is payable on top of their wages — not deducted out of.

Using tax tables to calculate wages

Each year, the ATO produces a range of tax tables to help you work out how much to withhold from payments you make to your employees. In our Ad Hoc Payroll Micro Course, we’ve already added the most current tax tables to the accompanying payroll spreadsheet, as well as the superannuation guarantee tables.

A HUGE PART of reconciling your bank account involves coding business expenses or purchases. You then need to keep a record of those expenses in the event you’re ever audited.

Our Xero Bank Reconciliations and Journal Entries Course covers how to code an expense or purchase in Xero, and it’s important to also store your receipts and get them to your bookkeeper if they’re working remotely.

Type the first 3 characters to discover courses, up-skilling programs and CPD articles.

EzyLearn's Career Academy

Enrolled into an EzyLearn course since 2013? Get access to new & updated course content and support by joining the EzyLearn Course Refresher Access membership Program. See how to extend your course life & support.

Xero is a great bookkeeping program for tradies who are on the go and using their phones (or a tablet) all the time. From receipts scanning to creating quotes and invoices, receiving payments and keeping track of project costs.

bookkeepercourse.com.au/produ…

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

A business’s balance sheet is a snapshot of its financial position at a particular period of time,

A business’s balance sheet is a snapshot of its financial position at a particular period of time,

Although the process of running a P&L differ between accounting software packages, they usually all contain the same elements, depending only on the business itself. In the first section, the cost of sales is subtracted from the revenue, which highlights gross profit. The business’ operating expenses are then subtracted from the gross profit, which leaves the operating profit. Now, all of the non-operating revenues and expenses must be factored into account, after which the business’ profit or loss will be displayed.

Although the process of running a P&L differ between accounting software packages, they usually all contain the same elements, depending only on the business itself. In the first section, the cost of sales is subtracted from the revenue, which highlights gross profit. The business’ operating expenses are then subtracted from the gross profit, which leaves the operating profit. Now, all of the non-operating revenues and expenses must be factored into account, after which the business’ profit or loss will be displayed.

Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.

Most businesses using an accounting program like MYOB or Xero will use the included payroll package to manage their employees’ payroll. For businesses with only a few employees, however, the additional payroll function is an unnecessary expense.