Someone made contact with us to find out which data entry and office admin courses they need to do to get a job using MYOB. It’s logical to want to know which courses will give you the skills for specific jobs so we put these guides together.

We’ve received lots of training course inquiries from new business in this last couple of months and a question that came up recently was “do you have a course that explains how much I can claim”. The person was asking about how much of the cost of their car can they claim as an expense because they use it for their business.

The answer to this question reminded me of how “flexible” the taxation laws are in Australia. You can “claim” any amount that you want and unless you are audited by the ATO you could possibly get away with it!!

The correct way is to determine how much of your costs are actually associated with your business and use that percentage. The ATO goes on to explain how to do this in detail.

One of Australia’s most popular small business accounting software has upped its pricing again, but with no new major added features for users (like when they included Hubdoc features in a previous hike).

Xero has announced that from September 1, 2022, three of its plans will increase in price, with the smallest increase at $2/month through to a $14/month hike.

So why are Xero prices increasing and what does it mean for users? Xero has some pretty expensive recent purchases, and their share price is still declining, so could this spell financial troubles for Xero?

The Australian government launched STP in 2016, where employers with over 9 employees must report their payroll information for each pay run to the ATO. When the ATO introduced STP Phase 2 earlier this year, some of the reporting obligations changed.

Here’s what you need to know about STP Phase 2 reporting in Xero, and how EzyLearn’s got you covered with the training.

If you’ve connected PayPal with Xero, and have been using it for quite a while, it might come as a bit of a surprise when you get an email from Xero telling you that your existing PayPal direct bank connection will no longer be supported and will stop importing transactions into Xero.

Why is Xero emailing you this? Especially considering there’s a timeframe in which you need to switch to the new PayPal bank connection, you’re probably eager to figure out what it all means.

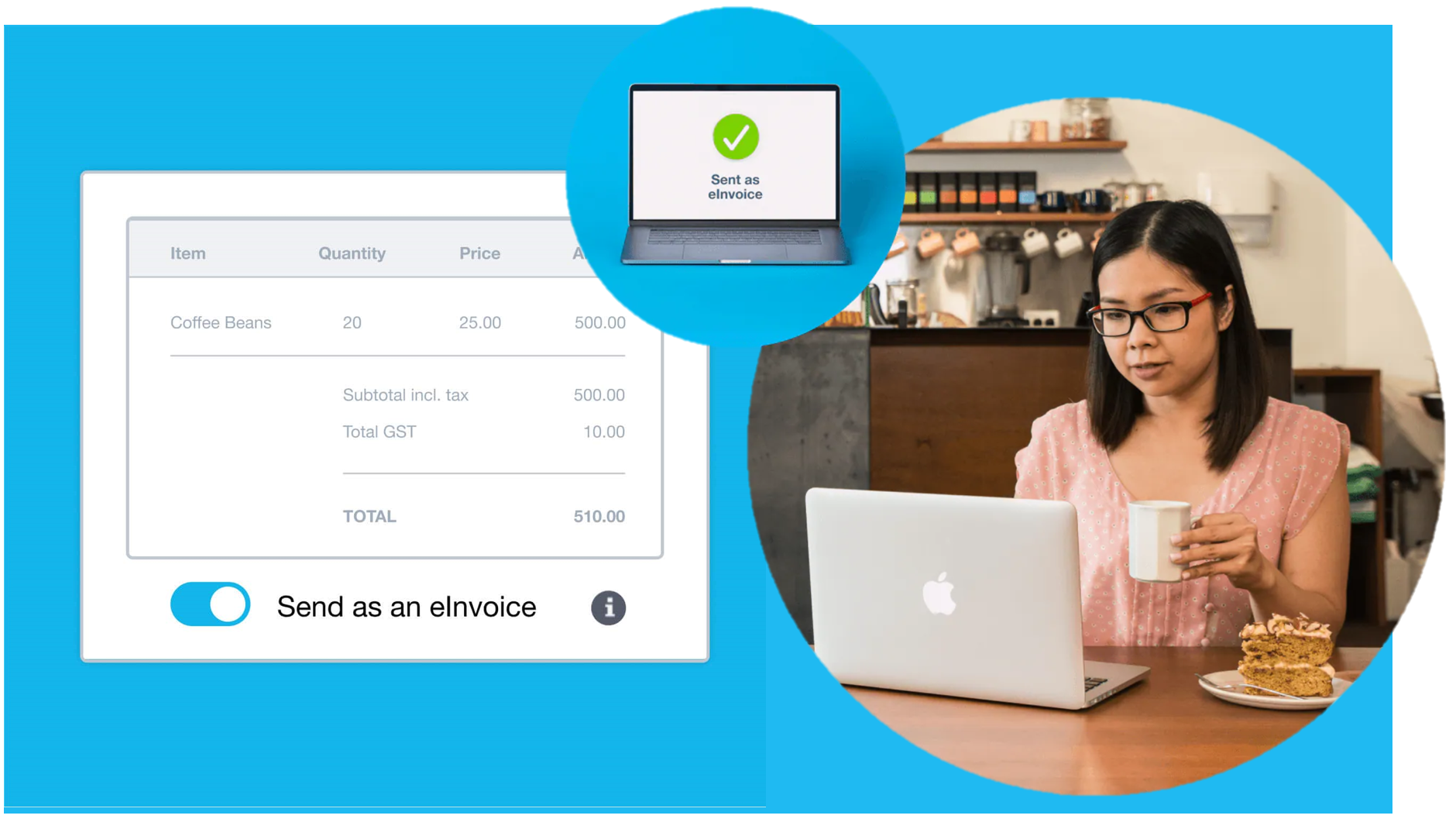

Invoices can be a hassle for both businesses and their clients. There’s nothing fun about chasing up that client about their late payment, nor is it an efficient use of time to trawl through emails and inboxes trying to find that invoice from however long ago.

The Commonwealth Government is pushing ahead with an alternative, that looks like it will make things a bit easier for everyone.

eInvoicing is on the rise! And since software like Xero has jumped in on the change, it’s important for small businesses to know what eInvoicing is all about:

It’s not a stretch to say the last few years have been tough…especially for businesses. Through lockdowns and restrictions we’ve seen businesses struggle, falter, adapt, and survive.

Now that we’re in to 2022, and things are (fingers crossed) almost looking normal again, it’s exciting to see how businesses will recover and thrive.

Xero has released a guide to small business trends for 2022, based on surveys they conducted in 2021 of their subscribers in Australia, New Zealand, the UK, Singapore, Canada, and the US.

Here’s are 10 trends on the rise for small business this year:

Did you know that Afterpay (and ZipPay) and some other Buy Now Pay Later providers decline sellers? Most Afterpay transactions are centered around the selling of physical products that change ownership from the merchant to the customer. This evidence is enough to bind customers legally, but what happens if you provide professional services like bookkeeping or accounting?

Accountants and Bookkeepers, like many other professional service providers including Lawyers and solicitors charge for their time or defined outcomes (like fixed fees for a certain number of transactions).

Will Afterpay take you on as a client? We’ve heard that many industries are rejected but there are alternatives and Xero’s App Store can help.

In our educational guide, Bookkeeping Beginner Basics, which you can download from the EzyLearn website for free, you’ll learn how to record journal entries in your accounting software, whether you’re using MYOB, Xero or QuickBooks. Most bookkeeping newbies don’t know what a journal entry is, though, which is what this blog post – the latest in our Bookkeeping Beginner Basics guide companion series – is going to help you to understand.

The journal vs. the general ledger

An accounting journal is the record that keeps accounting transactions in chronological order (i.e., as they occur), while the general ledger is a record that keeps accounting transactions by the account – see our previous post on the chart of accounts [Bookkeeping Beginner Basics: The Chart of Accounts] if you need help understanding what the term ‘account’ means in this context. Before computers, bookkeepers used to log all the financial transactions of a business in paper journals, and then at the end of the month transfer these journal entries into the general ledger, which was divided into various accounts that is now called the chart of accounts, and all the transactions were posted to these accounts using a method called double-entry bookkeeping.

Journal entries using accounting software

Today, however, accounting systems, such as MYOB, Xero, QuickBooks and the like, will automatically record most business transactions into the ledger immediately after the software prepares sales invoices, issues cheques to creditors, or processes receipts from customers, and as such you don’t have to create journal entries for most of your business’s transactions.

That being said, some journal entries still need to be processed, in order to record transfers between bank accounts and to record adjusting entries. You would need to make a journal entry, for example, at the end of each month to record depreciation or to record interest accrued on a bank loan.

Double-entry bookkeeping

If journal entries and general ledgers and the double entry bookkeeping method sound a bit too much, and you think you’d rather stick to the cash-based accounting method instead, prepare yourself for bad news: all businesses, whether they use the cash-based accounting method or the accrual accounting method, use double-entry bookkeeping to keep their books, and all accounting software applications, by default, are set up to adhere to the double-entry method, too. The double-entry bookkeeping method reduces errors and also ensures that your books balance, so as complicated as it may seem, it’s much easier in the long run.

If you still feel a little out of your depth, however, you can hire a reliable bookkeeper to manage your bookkeeping system and deal with all the journal entries and double-entry business for you, instead. Visit the National Bookkeeping website for to find a highly qualified bookkeeper whose experience and skills suit your business needs.

This blog post is part of our Bookkeeping Basics series, which are being published to complement our new educational guide, also titled Bookkeeping Beginner Basics, which you can download for free from the EzyLearn website.

But while there are close to a dozen cloud accounting systems on the market, most bookkeepers — thankfully — will only need to know their way around three: Xero, MYOB and QuickBooks. If you’re looking for a course or training resource on these programs we have a combo offer.

A lot of the time, however, people enrol in an Excel online training course or Xero online training course because they need to refresh a specific set of skills for their job, which means they don’t have the time to focus on other areas that don’t have an immediate relevance for their work.

Since then, however, a number of cloud-based accounting applications have entered the market — QuickBooks Online (now distributed by their US-based parent company Intuit), Reckon One, Saasu, Zoho, and so on.

Even though Xero was hailed as a breath of fresh air when it first entered the market, it is still a little more complicated to use when compared with other cloud accounting apps, like QuickBooks and Reckon One. For instance, the purchase orders feature is still hidden behind bills, when it could easily be access via a dropdown menu. But it’s not a major quibble.

Xero’s contact profile misses a beat

Although Xero allows you to assign customer numbers for your suppliers or customers in the contact profile, it doesn’t have the functionality to record customer numbers assigned by supplier or customer.

In MYOB, you must upload your bills to your in-tray, and then link them to your transactions. This is annoying, because it requires you to leave the transaction window and open the in-tray one.

***

Remember that when you select a cloud accounting package for your business, do not choose solely based on price. Make a list of the needs of your business and the functions you’ll require, and then select the accounting package that suits your needs the most. Ask your bookkeeper and other business friends for their recommendations as well.

Announcement: Microsoft Excel 2016 Beginners’ to Advanced courses now available!

At EzyLearn we include all versions of a software program in our training courses. That means when you enrol into Excel you get 2016 — AND — the older Excel courses which include version 2013, 2010, 2007 and even 2003 (if you really need it).

When you enrol in Lifetime Course Accessyou get access to ALL versions and ALL FUTURE VERSIONS as we continually update them — at no extra cost!

If using online reviews to help you work out what to buy, you want to make sure you’re really hearing it from the horse’s mouth, and not just reading fake marketing guff.

IF YOU’RE ANYTHING LIKE most people, rating and reviews are how you probably make many of your purchase decisions. This can be for purchasing white goods, clothing, a holiday, or even choosing a real estate agent.Continue reading Can You Trust Online Ratings and Reviews?

Buying a premises for your business need not be cost prohibitive and you may enjoy good equity growth.

IN OUR NEW CASH FLOW reporting, Budgets and ROI course for Xero, we delve into the purchase of real estate for your business, which you may use as office space or as a warehouse or as a storage facility and workshop, depending on your line of work.

Why some businesses don’t like buying

Lots of businesses avoid buying premises for their businesses, because you’ll need to have a large capital injection right off the bat, and you may also incur land tax obligations, building insurance, and also be liable for maintenance and repairs.

Renting gives businesses, especially new ones, flexibility, as you’re only locked into a short term lease — not a multi decade mortgage. And if you decide to move or find new premises before your lease term is up, you can often minimise the costs by subletting the premises.

You’re also afforded greater freedoms and stability when you own your business’s premises — in particular, protections from rising rents — than you would have if you rented your premises. If you outgrow the space, you can always access the equity and may be able to buy adjacent premises, or rent out your existing ones while you upgrade, providing another valuable income stream.

Industrial units are a good pathway into ownership for your business. If you don’t need to be right in the heart of the city or major town centre, you can often purchase an industrial unit for under $100,000.

In Newcastle in the Hunter region of New South Wales, you can purchase an industrial unit called a Cubbyhole, which can be used as a workshop, storage unit or office space for tradespeople, small and online businesses. These come with amenities such as toilets and showers, car parking (including visitors’ and disabled) and CCTV security, among other things and are worth checking out if you want to buy and only need a smaller business space.

Cash flow reports show the money going in and out of the business, so they’re better indicators of a business’s overall financial health than a Profit and Loss statement (P&L).

A cash flow report enables you to make forecasts and budgets for your business based on previous trends — recurring expenses, average time to get paid, seasonal quiet periods, and so forth.

The 3 cash flow categories

Cash flow reports are typically broken up into three categories:

Operating activities: cash flowing in and out of the business from revenue-generating activities

Investing activities: cash flowing in and out of the business from the acquisition and sale of long-term assets

Financing activities: cash flowing in and out of the business from borrowings and changes in equity.

Items in a cash flow report

In our Cash Flow, Budgets and ROI Xero Training Course, you’ll learn how to generate a cash flow report in Xero. That report will show every transaction that’s run in and out of your business, divided among one of the three categories.

In the operating activities category, you’ll typically find things like costs associated with any training courses or seminars, advertising and marketing expenses, income or commissions from your business, subscriptions to any magazines or periodicals, etc.

Under the investing activities category, you’ll find the cost of purchasing office or warehouse space and the capitalised borrowing cost, for example.

The financing activities category will show the loan you’ve taken out to purchase your business’s office or warehouse space.

The sales spiels of many of the notable online accounting software packages like QuickBooks, Wave Accounting, Outright, Kashoo, LessAccounting, Clearbooks and even Xero, claim that this feature will save you time and effort as it imports your bank transactions. The truth is, this is not foolproof and won’t work 100 percent of the time (even if it’s just a matter of not being able to get your software and your bank to “connect” just as your mobile phone connection inexplicably doesn’t work sometimes).

Therefore, always double check your bank transaction data has been imported accurately. This said, importing your bank statement into Xero (or whatever accounting software you use) is a really important step in the bookkeeping process that a lot of business owners forget or don’t know how to do. And the technology is only going to get better!

Using the correct format

To import your bank statement into Xero, you must ensure it’s in the correct format. Xero can only work with a CSV file of your bank statement. Depending on your bank, you might be able to download your bank statement as a CSV file from your internet banking, or you will have to create one from scratch.

Creating one from scratch isn’t too difficult. If your bank doesn’t give you the option of downloading a bank statement as a CSV file, you can create one yourself in Microsoft Excel.

You can download an Excel template from Xero. It includes the recommended fields and is already set up as a CSV file, so all you need to do is add in your data.

Set transaction rules

Once you’ve created and uploaded your bank statement to Xero, you’ll need to set up transaction rules for recurring expenses. You’ll learn how to do this in our Cash Flow Reporting, Budgets and ROI Xero Course.

Setting rules for recurring transactions helps speed up the reconciliation process, which depending on the type of business you operate and how often you reconcile your account, can be the most time-consuming part of the process.

Importing your bank statement and creating rules for transactions that occur each week, month fortnight, year, etc, greatly speeds up this process.

No CSV? Use bank feeds

If your business has lots of expenses every week, and your bank doesn’t let you download your bank statement in a CSV format, you may find that manually creating one in Excel each month is too time consuming.

Set up bank feeds instead. Bank feeds is the process of linking all of your business accounts, whether they’re credit cards or bank accounts, to your accounting software, so that each time you make an electronic purchase, it’s automatically imported into your accounting software.

This will allow you to reconcile your account each fortnight, week or more frequently, if you desire, than once a month when your bank statement comes in.

Learn Microsoft Excel from scratch or brush up your Excel skills, at your own pace, with our affordable Excel online training courses — where you get THE LOT (that’s 9 courses in total) for ONE LOW PRICE — everything included! Volume corporate discounts are available and our courses count towards CPD Points. NOW is the time to learn to use Excel, one of the most-used software applications in the world.

Search this site

Type the first 3 characters to discover courses, up-skilling programs and CPD articles.

EzyLearn's Career Academy

Enrolled into an EzyLearn course since 2013? Get access to new & updated course content and support by joining the EzyLearn Course Refresher Access membership Program. See how to extend your course life & support.

Xero is a great bookkeeping program for tradies who are on the go and using their phones (or a tablet) all the time. From receipts scanning to creating quotes and invoices, receiving payments and keeping track of project costs.

bookkeepercourse.com.au/produ…