It can be easy to lose track of separate income streams; Excel is a great tool for monitoring which work your income is coming from.

IF YOU’RE AN INDEPENDENT contractor, or you’re a full-time employee about to start up a side business, then you need to be able to keep a good track of all your income streams. There are a couple of reasons for this and both of them relate to tax. Continue reading What to Do When You Have More than One Income Stream

There’s more to profit and loss than meets the eye: Sometimes a company’s losses outweigh its revenue, but it doesn’t mean that company is in a bad position.

It’s not the most detailed financial report, probably because the company itself is still in its early stages — there’s actually a good argument against early stage ventures listing on the stock exchange, but that’s fodder for another post.

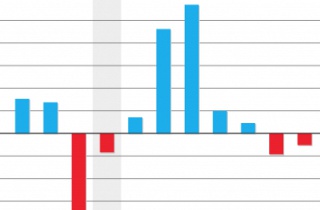

Revenue vs. losses for the period

The good news for BuyMyPlace is that its revenue increased 129 percent on the prior comparative period (PCP) to $1 million for H1 FY16/17, up from $133,518 in H1 FY15/16.

That’s an impressive leap in revenues in just 12 months, however, the BuyMyPlace financial results also reveal that the business made an even greater loss of $1.7 million, an increase of 1205 percent on the PCP.

A closer look at the report shows that, while the losses increased more than a thousand percent, it was due to an increased investment in marketing and advertising — principally on TV spots which totalled $517,723 compared with $98,578 the year prior.

This resulted in an 80 percent increase in the number of listings on the site (that is, the number of people using BuyMyPlace to sell their home), while order value increased 27 percent (people who were choosing more expensive packages).

BuyMyPlace is in good health

Although this business recorded losses that outweighed its revenue, BuyMyPlace is still in good financial health.

The report also shows that it has over $4 million in cash and cash equivalents, and only a little over $600,000 in liabilities. Although the liabilities have increased, it’s not due to taking on any additional debt — indeed, BuyMyPlace has paid down all of its loans — but was instead due to a 786 percent increase in staff salaries and, as a consequence, an increase in staff provisions and benefits — i.e., sick and annual leave.

Strategy for future growth

Not many homeowners actually want to sell their properties themselves — one estimate puts it at around 7 percent of the total number of homeowners. However, most people do want greater clarity around how the process works (including fees and commissions) — even if they still want assistance selling their homes.

Perhaps realising this, or perhaps in response to increased competition in the fixed-fee real estate services (see: Purplebricks, Settl, etc), BuyMyPlace also launched its own full service package, giving homeowners access to a real estate agent to sell their home for a fixed fee.

This will enable BuyMyPlace to capture a greater volume of homeowners, who are looking for a low cost alternative to sell their homes, but who don’t want to do it entirely themselves.

The other strategy for growth: increasing listing depth revenues.

At some point, BuyMyPlace will stop growing its market share. Or, in other words, the market of people looking for a low-cost option to sell their home will be tapped out.

But as a business, and as a publicly listed one, BuyMyPlace will need to keep growing its revenue, not merely keep it steady. It’ll need to do as other real estate services, such as REA Group and Domain have done, and increase listing revenue depths, by selling more expensive packages to customers.

BuyMyPlace will need to find additional value it can sell to customers, without necessarily increasing its own expenses to do so — or putting up its prices, which a business can usually only do once it’s cornered about 65 percent of the market, and BuyMyPlace is a long way off that yet.

***

That’s a lesson for every business owner out there. And it’s something we cover in our online Business StartUp Course.

You’ll learn how to run and understand the financial reports for your business in our Xero and MYOB training courses. You can also learn about strategies for business growth in our Business StartUp Course. Or for more information, visit our website.

The simple act of creating an Excel spreadsheet to itemise your expenses can help you keep track of everything eating into your business’ cashflow – even if not strictly deductible.

HAVE YOU RECENTLY STARTED running your own business? Whether you have, or whether you’re about to, reconciling your bank accounts regularly is probably one of the best ways to monitor your expenditure in relation to your income.

Your accounting software will help you to keep track of your income and business expenses and other important things that will affect your start up — such as how long it takes to get paid — while an Excel spending or expense sheet will help you to monitor all of your spending, business or otherwise.

The bank reconciliation process

This starts when you get your bank statement, but you can speed the process up, by entering recurring expenses into your Excel spreadsheet as they occur.

In your Excel spending sheet, you’ll enter the expense in total, but in your accounting software, you’ll only enter the percentage of the expense that relates to your business.

Identify cash flow problems

If your business has poor cash flow, using an Excel spending sheet in addition to your accounting software will allow you to identify what’s causing your cash flow problems. Sometimes cash flow problems are caused by later payers, due to poor credit management processes. Other times, however, you may find that you’re simply not earning enough to cover your expenses each week or month.

To remedy this immediately, you should look through your Excel spending sheet and see if there are any expenses, either business or discretionary ones, that you can reduce or eliminate. Then you should work on increasing your income. That’s easier said than done, which is why you should reduce your spending first.

Forecasting profit

If you don’t identify any cash flow issues, you will be able to begin forecasting profit. Typically, profit just refers to the income left over after all your business expenses have been accounted for.

But there are plenty of start ups and sole traders, who have a profitable business but are not profitable themselves.

That’s because there are many other expenses in your ordinary life — the remaining 70 percent of your internet bill, for example — that you still need to pay for.

If you’re also recording all your other expenses in an Excel spending sheet, you’ll be able to forecast your business’s profit, as well as your own personal profit (otherwise known as savings) with much greater accuracy.

The chart of accounts

In effect, what you’re doing here is creating a chart of accounts. You’ll learn more about the chart of accounts in our Xero and MYOB courses, but they are, in a nutshell, a financial record of every account — asset, liability, equity, revenue, etc — in your business.

Why Excel is Great for Keeping Track of Your Spending if You’re Self Employed

That take away coffee that you buy each morning should be added to your business expenses sheet; even if not claimable it shows where your money is going.

WHETHER YOU’RE ABOUT TO start your own bookkeeping business, or whether you work as an independent contractor (even if you’ve been doing this for a while), it’s really important to know how much you’re spending each month.

Your Xero, MYOB or QuickBooks accounting software will help you with some of this, but the very best way is to create an expense or spending sheet in Excel — which we teach you how to do in our Excel training courses — as this gives you a far more detailed look at your expenses and spending.

Not all your expenses are 100% business ones

Sometimes you can’t claim 100 percent of your expenses as business ones — the costs of running your car, home internet, rent, utilities, etc — but you should nevertheless keep track of your spending on these items because it will affect your cash flow.

That’s why keeping an Excel spending or expense sheet is a good idea for contractors and home-based business owners. You don’t want to enter your home internet into your accounting software as a business expense, if only 30 percent of it is used for business purposes, but you still need to keep track of it, so you can manage your cashflow.

Monitor frivolous spending

One of the things we love about using Excel to track your expenses and spending is that every little expenditure is right there, in plain view.

This isn’t the case with Xero or MYOB or other accounting software. Your expenses are hidden away, and you have to run a report to get a good breakdown on where your money is going.

Not so with Excel,. If you buy a coffee every morning, it’s right there, in a category you can label as “coffee”.

Now, we’re not saying that coffee is frivolous. Far from it. Many of us need coffee just to function (!) but there are lots of small things we spend money on every day, week, month that add up. When you’re self-employed you need to keep an eye on these “little” things.

Sometimes, you’ll find that you’re spending lots of money each month on subscription services that you’re not even using. Eliminating $15 a month here and there makes a big difference.

Create as many categories as you need

That’s the other great thing about using Excel to track your spending: You can create all the expense categories you like.

Of course, not everyone wants to track each and every expense right down to their last bag of jelly beans — that actually would be a little ridiculous — and for most the most part, you can lump your groceries into a category for discretionary spending, but there are some things you might want to separate out — movie tickets, money spent on lunches and dinners, and so forth.

These things tend to add up, and if you want to keep an eye on them, separating them out is the easiest way to do that.

Back to those business expenses

Each fortnight or month or however regularly you complete your bookkeeping, you can easily add in those business expenses into your accounting software — or your bookkeeper can.

Remember, if you spend $60 a month on internet, but only 30 percent of its use is for business purposes, you should only add $18 a month as a business expense in your accounting software. In your Excel expense or spending sheet, however, you’ll put the full $60 in, as you need to have the money in the bank to cover this expense each month.

***

You can learn how to create and manage your expenses or spending in our Excel training courses, where you’ll be able to create your own spending or expense sheet. Visit our website for more information.

We feel your pain! Often businesses lack the cash flow to make super payments, but you always have to pay them in the end…

WHEN YOU’RE SELF EMPLOYED you are responsible for managing your taxes and your superannuation — the latter of which many business owners let go by the wayside. It’s almost always because they don’t have the cash reserves to contribute to their super fund regularly enough.

Just as you would create a budget to make a business investment or asset purchase, you can use Xero and Excel to determine how much super you should contribute on your behalf, and then make the payments.

Run a cashflow report

You’ll learn how to run a cashflow report in our Xero training courses. This report will show you the periods when cashflow is liquid and when it isn’t. Run a cashflow report for a couple of different periods, and export them into Excel. This will give you a better idea of trends and cycles in your business.

You can also use a cashflow report to determine your income before taxes, expenses, and so forth. Superannuation is determined based on gross earnings — or revenue — so you should use this figure to work out your super contributions. This is especially important before end of financial year!

Determine super contributions

At time of writing, the superannuation guarantee is 9.5 percent of your gross revenue, before taxes, expenses, etc. If you set your prices correctly, you should have already factored this 9.5 percent into your prices or hourly rate. If you haven’t, you ought to consider revising what you charge customers and clients.

If you were an employee of a business, your employer would be required to make super contributions on your behalf, at least each quarter. Because you’re self-employed and self-managing your super contributions, you can make them as frequently or infrequently as you like, so long as you’re contributing the correct amounts. (Speak to your accountant or financial advisor, however, if you’re salary sacrificing above the minimum amount — this may affect your tax.)

Make super contributions

Once you’ve determined how much you should contribute to your super fund each quarter, refer back to your cashflow report and to the periods where your cashflow is especially liquid. Are you able to make your contributions each quarter easily, and without compromising your business’s liquidity? Would it be easier to make smaller, more regular contributions?

The decision is yours.

Use Xero to make your super contributions. Xero is connected to a superannuation clearing house, and if you’ve been using to Xero to pay yourself a wage, it’s the easiest way to do so. If you’re not using your accounting software to pay yourself a wage, you can make the payment directly out of your bank account, however, you’ll need to track this in Xero for taxation purposes.

***

Our Xero training courses will show you how run cashflow reports and make wage and super payments, while our Excel training courses will also teach you how to create business budgets and forecasts. Visit our website for more information.

It’s a real buzz when you learn something new: a great way to up-skill your staff members and keep people interested at work is to provide them with online training course material.

OUR MYOB TRAINING COURSE is basically an induction into the role of a bookkeeper, in that it provides students with an overview of the duties typically carried out by a bookkeeper. Most of our students take our MYOB training course because they both want, and need, to know how to use the software in order to find work as a bookkeeper.

In the world of business training and coaching, this is called the Will versus Skill Matrix. Employees who have both the will to succeed and the skill to succeed are highly desirable in the workplace.

Transparency, will and skill

Employees who have only one of those attributes, however, are less desirable. Helping staff maintain both the will and the skill to succeed in their jobs has a lot to do with how transparent you are as an organisation.

We’ve mentioned transparency in business before, notably in relation to induction training programs. Induction training programs are a highly efficient way to communicate easily and efficiently with your staff, while also testing their will and skill to succeed at their jobs.

While most induction training programs are used to merely address the requirements of the Work Health and Safety Act, or to induct contractors and consultants to a business’ premises, induction training programs can also be used to further your employees’ professional development.

Help your staff upskill with a Word or Excel course

Furthering your employees’ professional development can be done by providing your staff with online training courses that are relevant and useful to their jobs, such as a Word or Excel training course. You’ll be surprised how many tasks can be done with these software applications — and therefore how empowering this knowledge becomes!

Online delivery of this content allows your staff to complete the course at their own pace, in an informal environment — at home or at their desk at work, rather than in a dedicated training centre on a dedicated day — and it also allows you to monitor their progress.

Being able to see how your employees are getting on with the training courses can illuminate areas where your staff could benefit from further training; it can also highlight those staff member who possess the will and the skill to succeed.

Those staff members who are have both the will and the skill to succeed in their jobs also happen to be highly engaged, and as we mentioned in a previous post, more productive.

***

If you’re looking for ways to keep your staff highly engaged with your business, we can help you tailor and deliver highly engaging induction training courses to your staff. Visit our website for more information, or contact us today for a quote.

We mentioned that Jerry should use his accounting software to determine whether his he’ll have the start-up capital required to fund his new venture for the next 12 months. The best way to do this is to create a cash flow forecast, and we’re going to show you how.

Cash flow is a better indicator of available funds

If you’re wondering why you wouldn’t create a profit forecast, it’s pretty simple. Cash flow represents money in the bank, after you’ve paid all your suppliers and staff and loan repayments and so forth, while profit just shows how much the business earned but doesn’t take into account any cash outlays.

Profit just shows how much the business earned but doesn’t take into account any cash outlays.

It’s important to understand that it’s not uncommon for businesses to be profitable; however due to cash outlays, these same businesses may not actually have enough money in the bank to fund investment, or in this case, a new venture.

Generating a cash flow report in Xero

Follow these steps in Xero to generate a cash flow report for your business:

Go to Reports, then click All Reports.

Under Financial, select Cash Summary.

Enter the following report settings:

Date — The latest finalised month

Period — 1 month

Compare With — Previous 11 Periods

Select the Include GST and Show YTD filters

Click Update to generate the report in Xero

At the bottom of the report, click Export and select Excel to download the report in Microsoft Excel format.

The messy startup needs Xero Cashflow Training

There is a great business case study with lots of practical exercises in the Xero Cashflow Training Course. You’ll learn how to code and manage lots of different types of transactions and reconcile 2 quarters worth of transactions and end up producing cash flow reports to make financial sense of it all.

You’ll even be able to highlight alternative ways of financing some of those transactions.

Set up formulas to forecast 12 months ahead

In Excel, you’ll need to create formulas that will show you the average cashflow of your business across the previous 12 month period, so you can then forecast ahead for the next 12 months.

If you don’t use Xero and you’re using MYOB or QuickBooks, our MYOB and QuickBooks training courses will also show you how to run cashflow reports, among many others.

Documenting and tracking your business premises’ expenses leads to accurate tax and activity statements.

IF YOU DECIDE TO buy your business premises it will have an effect on your tax. Our Xero training courses will show you how to account for your business premises, but here is what you need to consider about your tax and GST obligations.

Capital gains tax (CGT)

If your business will be operated out of the premises you buy, it will be subject to CGT when, or if, it is later sold. As such, you need to keep records about when and for how much the property gained so you can work out the capital gains when you sell it.

Capital gains occurs when the amount the property is sold for is greater than what it originally cost to acquire it. If the property is sold for less than its original purchase price, this is known as a capital loss.

Capital losses

If you make a capital loss when you dispose of the premises, you can use that loss to reduce any other capital gain you might have also made in the same year — another property or shares in another business, say.

If you haven’t made a capital gain in the same year, you can use the capital loss to reduce a capital gain in a later year, but you cannot use a capital loss for any other income.

Income tax deductions

If the premises is used to run a business, or is available to rent for that purpose, you can claim tax deductions for expenses associated with owning it; such as interest on a loan to buy the property and maintenance expenses. Keep records of your expenses from the start, so you can claim everything you’re entitled to.

GST

If you buy commercial premises, you may be eligible to claim a credit for the GST included in the purchase price. Additionally, you may also be able to claim GST on other expenses that relate to buying the property — such as the GST included in solicitors’ fees and ongoing running expenses.

However, you can’t claim GST in the following instances:

The seller used themargin scheme to work out the GST included in the price

You purchase property from someone who is not registered or required to be registered for GST

You purchase the property as a GST-free supply

You’re not registered for GST.

Keeping track of the purchase and expenses related to your business premises properly in your accounting software is vital to the ongoing financial health of your business — and accurate tax and activity statements.

Struggling to manage your online payroll management? Our Xero and MYOB courses will help you get the most out of this software so you can manage payroll in house.

MANY COMPANIES OUTSOURCE PAYROLL because it contains many moving parts. For instance, there’s the payment of wages each week or fortnight or month, sure. But there’s also superannuation contributions, PAYG obligations, annual and sick leave accrual.

Fortunately, most accounting apps like Xero and MYOB have made payroll easier to manage, particularly if you only have a handful of employees.

Superannuation clearing houses

Nearly every major cloud accounting package has a connected superannuation clearing house within its payroll package. Xero and MYOB are both SuperStream compliant, a government initiative to help business owners tell which accounting software apps will let them make electronic superannuation payments. And QuickBooks uses a partner payroll system which is also SuperStream compliant.

Batch wage payments

Electronic superannuation payments are one way that paying staff is made easier, but paying a dozen or so employees individually each week or fortnight can be tedious. Fortunately, both Xero and MYOB have a ‘pay run’ function that lets you make batch wage payments. This eliminates the tedium of paying employees individually, as well as the potential for error.

Accounting software calculates entitlements

MYOB, Xero and QuickBooks, if you’ve set up your employees correctly and have the appropriate payroll subscription, will also calculate your employees’ sick and annual leave entitlements, also reducing the time it takes to process payroll and the potential for error.

EzyLearn courses now include real life case studies

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our Excel Ad Hoc Payroll case study which is part of our Intermediate Excel Online Training Courses. Where possible, we draw on real-life case studies as examples, to help you learn, and apply your skills, in a relevant way that makes sense. Visit our Micro Courses page to learn more.

Documenting procedures helps keep your bookkeeping up to speed

Rescue bookkeeping is not ideal – it’s often expensive and shows you’re not in control. A bookkeeping procedures manual will outline what bookkeeping needs to be done, when.

IN A PREVIOUS POST we talked about how to tell when you need rescue bookkeeping, which is basically when a business is behind on its bookkeeping by three months or more and the deadline is looming to lodge their activity statements.

Rescue bookkeeping work costs more than having your bookkeeping taken care of regularly, because it’s often messy and there are no procedures in place to manage the bookkeeping efficiently.

What’s a bookkeeping procedures manual?

A bookkeeping procedures manual clearly identifies the regular tasks and activities your bookkeeper needs to take each week, fortnight, month or quarter to ensure your bookkeeping is kept up-to-date. This not only gives you the peace of mind that your bookkeeper is staying on top of your books, but it also helps you to understand what’s going on with your business.

If you require regular P&L statements or balance sheets, having a procedures manual to clearly outline how frequently they’ll be created helps you to stay on top of your business’ financials.

A typical procedures manual will include:

Simple steps that are easy-to-understand and succinct

Tasks are written up in a step-by-step style, so they can be followed logically

References, links or examples are included to help readers understand

Contain a number of formats — written steps, flow charts or checklists.

Rather than leaving your bookkeeping to the last minute, so you’re always operating your business in dark, organise to have bookkeeper create a procedures manual to regularly take care of your business’s bookkeeping.

We Can Help You Find a Good Local Bookkeeper

We have bookkeepers, BAS agents and accountants located across Australia, available to help businesses in need of rescue bookkeeping work. Visit our online bookkeeping directory, National Bookkeeping, to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

Go to National Bookkeeping for more information, to see our rates or to request a quote.

Dive deep into your claimable expenses and don’t forget all those smaller prepaid expenses like magazine subscriptions or domain name registrations – you can only claim all of these during the period in which they occurred.

WE’RE IN THE LAST QUARTER of the 2016/17 financial year, so now is the time to dive in deep and check you’ve included every single business expense — prepaid or otherwise — to ensure all your expenses are in order.

We all know this, but remember, they can only be claimed for the period in which they occurred. If you forget to claim a major business expense in the financial year that it occurred, you can’t make it up by claiming it the next year.

It’s really important you thoroughly check your credit cards and business accounts to make sure you’ve accounted for each expense. The final quarter of the financial year is also a good time to make any purchases for your business, because you can claim them straight away.

Prepaid expenses are often forgotten

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

These deductions are often prepaid and may not come up on your radar and may certainly not show up on your final quarter bank statements.

Make a list and check it twice

Over the next month or so, make a list of all of your expenses as you think of them. This makes it easy to spot them when you’re going through your bank and credit card statements and checking them against the expenses in your accounting software.

Want to make your business presentations and publications more eye catching?

Gone are the days of excruciatingly dull PowerPoint slide presentations. Nowadays PowerPoint is the hidden gem used to generate animations, videos, movies, advertising and graphics. It’s a great ally to the marketer or social media person in your organisation.

Depending on the structure of your business, you may be legally required to include a P&L statement with your tax return or activity statements. Your tax agent will be able to advise you if your business will be required to file a P&L, which requires all of your bookkeeping to be up-to-date before you can run it.

Even if you don’t have to file one with your activity statements or tax returns, it’s still a good idea to run a P&L for your own sake. A P&L statement identifies whether your business has made a profit or loss and which accounting period these occurred.

Accounts receivable, payable

Find out who owes money to your business and to whom your business owes money. This is obviously part of the credit management process, which any good business will have in place already, but it’s a good idea to keep a steady eye on what’s coming in and what’s going out as EOFY approaches.

PAYG, superannuation

The end of each quarter brings a lot of PAYG and superannuation reporting, but EOFY brings a double whammy of activity statements tax returns and PAYG and superannuation compliance. You’ll need to run these reports so your bookkeeper can complete the payroll component of your returns.

Inventory stocktake

If you sell goods, you’ll need to complete a stocktake of your business’s inventory so that any missing stock can be written off, and to ensure you’re starting a clean slate for the new financial year.

We show you how to write off stock and inventory before the EOFY

Do you know how to make inventory adjustments? Our Xero and MYOB BAS and GST Reporting courses can show you how.

IT’S A GOOD TIME TO START looking at any slow-moving or obsolete stock that your business (or your client’s business) may be holding, as we’ve reached the end of Quarter 3 and have now started Quarter 4 for the 2016/17 financial year — which means the end of the financial year is fast approaching.

Writing off stock in MYOB or Xero is known as making an inventory adjustment, and our MYOB BAS Reporting and GST or Xero GST, Reporting and BAS training courses take you through the steps to do this. But first, you need to identify which items aren’t selling. We’ve created this case study to help you understand how.

Understanding your inventory’s performance

Every business needs to understand how their inventory is performing, and how it impacts their business. If the business owner is too busy to stay on top of this, then they should employ a bookkeeper to help.

A good example of why understanding inventory is important to a business is to look at an air conditioning company. This business makes money two ways:

Selling air conditioning units

Installing / maintaining air conditioning units

The margin on the sale of an air conditioning unit is not much, a few percent on top of the wholesale price. Where the business makes its money is in the installation or maintenance of the units it sells.

The business purchases three dozen units, of varying brands, models, price points, etcetera. It now needs to know which units are most popular with customers and why; which units aren’t popular with customers and why; whether it’s profitable for the business to continue to stock the unpopular units; or, conversely, whether it’s profitable for the business to continue stocking the popular units.

Inventory reporting

The business’s bookkeeper regularly runs a number of reports in their accounting software, including profit and loss reports and stock-on-hand reports. These reports are used to identify which units sell quickly, as well as the units that take longer to sell, and the profit margins on each.

The units that sell quickly don’t require a technician to install them. Although they’re responsible for the majority of sales, they don’t generate more revenue for the business. The units that sell slowly, do generate more revenue as they require installation and maintenance, however too many units were ordered and they’ve now been discontinued by the manufacturer. Some units have hardly sold, and, although not discontinued, have been superseded by newer models.

Stock write offs and future orders

Because the bookkeeper regularly runs these reports, s/he has been able to export them into Excel for further analysis. By the end of Q3, the bookkeeper can make suggestions to the business owner about the future of the business.

In particular, the bookkeeper suggests that the units that have been superseded are marked down to clear as much stock as possible, and cease any new orders. Likewise, the discontinued models will be marked down.

Orders for the units that replaced the discontinued models will halve the order volume. Likewise, order volumes for the top selling units will reduced. The profit margin on these units is very low and they result in no additional revenue from installation or maintenance. The profit that would be earned on the additional units is negligible, however by reducing the unit volumes, the business improves its cash flow.

Act NOW for EOFY

If your business sells stock or a combination of stock and services, like the air conditioning business does above, start looking at your inventory now. Markdown any slow-moving stock at the end of Q3, to give your business time to move the remainder of it. If it doesn’t sell, write it off at EOFY.

We feature our own online directory of local bookkeepers looking to add to their customers. Visit National Bookkeeping to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

A Chattel Mortgage Can Help Keep Your Business Cashflow Under Control

A chattel mortgage can tide your business over without having to dip into savings.

In our Xero Daily Reconciliations Course, you’ll learn how to set up a chart of accounts, among other things such as running balance sheets and Profit and Loss (P&L) statements. For the most part, daily transaction reconciliation is pretty straightforward, until you get to a capital purchase, which, if it’s over $20,000 or was purchased prior to May 2015, needs to be dealt with differently.

In most cases, when a business purchases major assets, such as a motor vehicles, it’s known as a capital purchase, which is made via a loan. There are two types of loans the business can take out: a hire purchase loan or a chattel mortgage.

Buying assets on hire purchase

This is an agreement between you and the lender to acquire a motor vehicle. During the hire period, the lender legally owns the car and you pay regular instalments to the finance company. For tax purposes you can claim depreciation, running costs and interest paid against your business income. When you pay off the loan in full, legal ownership is then transferred to you.

Buying assets on chattel mortgage

Chattel mortgage is essentially a mortgage over goods to be financed. Chattel mortgage is classed as a cash sale in that the goods automatically become your property on purchase and the finance company takes a mortgage over the chattels.

Just as a hire purchase you can claim depreciation, running costs and interest paid, against your business income. The chattel mortgage allows businesses to claim the full input tax credit from GST incurred expenses immediately (next BAS statement).

Chattel mortgages are more popular

Chattel mortgages became popular when BAS and GST was introduced, because businesses could claim the GST at the time of purchase, whether they ran a cash system or an accrual accounting system. Plus, under a chattel mortgage, the allowable depreciation and interest payment are also tax deductible.

How capital purchases affect cash flow

If a business doesn’t take out a loan to make a capital purchase, it will have to dip into its savings, which can adversely affect cash flow, especially on big ticket items. Taking out a chattel mortgage, however, helps to keep cash flow under control because the business can borrow the funds (and claim the interest back as a tax deduction) without any major impact on cash flow. You will also then be able to factor the repayments into your monthly forecast projection.

Why It Pays to Call the Switchboard When Doing a Reference Check

How do you really know the mobile numbers provided for references truly belong to who they say they are?

I recently had a conversation with a colleague who said she’d never once been asked to produce a copy of her university degree or her transcripts, despite stating on her resume that she’d graduated with a high distinction average.

Gee, I thought, not once? Not a single recruiter or employer had ever requested a copy of her degree? I found this fact astonishing, particularly since more professions require, by law, certain qualifications — as BAS agents are, for example. So how people know my friend wasn’t fibbing in her credentials? Fact is, they didn’t.

Check, even if you use a recruiter

I wrote a blog some time ago about recruiting on LinkedIn and why it’s so important to check references for yourself. People often underestimate the importance of checking a person’s credentials, so long as they get a reference from their last employer. Often, though, most people only provide a mobile number for their references, so whether you’re speaking to the candidate’s former employer, a co-worker, or their mum is sometimes anyone’s guess.

I was reminded of how important reference-checking is again, when I was reading a couple of articles on Longreads, and I found myself utterly fascinated by two of the biggest cases of journalistic fraud ever committed (though I admit to having never heard of them before the weekend, despite one occurring more than 30 years ago).

Sometimes people don’t just lie on their resume

In the first instance, a journalist named Janet Cooke fabricated a story for TheWashington Post about an 8-year-old heroin addict. She won a Pulitzer Prize for it in 1981, and then had to give it back when it came out that there was no such 8-year-old. In the second case, Jayson Blair, a journalist for The New York Times, was found to have fabricated or plagiarised 36 out of 73 stories written over a 6-month period, in what turned out to be the biggest scandal in the newspaper’s hundred-plus year history.

What I found most intriguing, though, was that neither Cooke nor Blair had been properly vetted before their employers hired them. In fact, it was Cooke’s falsified resume that was ultimately her undoing when, after receiving the highest honour in the field of writing, a former employer noticed something was amiss with her Pulitzer biography — her education and professional achievements had been grossly overstated. (Rather ironically it was Bob Woodward, of Woodward and Bernstein — the journalists who uncovered the Watergate Scandal — who signed off on hiring Cooke.)

The same would prove true for Blair, who, it turned out, never graduated from university, and had a murky work history with the Times’ sister publication, The Boston Globe, where his superiors had been less than impressed with his less-than-high standard of work.

(Of course, the equally interesting case of Australian author, Helen Demidenko, who won the Miles Franklin Award in the early 1990s, only to later be dubbed by the Sydney Morning Herald as a ‘literary hoax’ also springs to mind.)

Benders-of-truth almost always get caught

Plenty of people lie or embellish on their resumes, and while a good majority of them go unnoticed, others are caught out — sometimes very publicly, and often only after the organisation has been very publicly embarrassed, as in the case of Cooke and Blair.

My advice, then, is to always check the references of new hires meticulously. Rather than calling the mobile numbers or direct lines of the candidate’s references, call the main switchboard and ask to speak to that person’s manager or superior.

And always ensure to ask for a copy of any credentials, like university degrees. If you’re employing someone where, by law, they’re required to hold a certain qualification — as is the case for BAS agents, for instance — it’s imperative you can verify the person’s credentials.

Excel Will Help You Work Out the HOW of Depreciation

We recently updated our advanced Microsoft Excel Training Course content. It now contains a case study, by way of an extra exercise workbook, using a granny flat building project to create a financial forecast.

We chose a granny flat building project for our case study because it’s an investment decision quite a lot of people with or without a business have made. It’s also a capital asset that can be depreciated over time. Therefore it has the potential to affect your taxes in lots of different ways.

Your bookkeeper uses Excel to calculate depreciation

When you build a new structure, such as a granny flat, which you intend to rent out or use for businesses purposes — i.e., it’s an investment and not for your own personal use — the building can be depreciated along with some of the fittings and finishes (floorings, curtains, paint, etc). That’s despite the value of the land upon which the granny flat is constructed increasing in value over time.

Excel will calculate the depreciation amounts for you, which you should then enter into Xero. We cover how to deal with depreciation in our Xero Bank Reconciliation Course, because lots of businesses own, or will own, a capital asset at some point.

However, this doesn’t tell you how to determine the depreciation amounts, which most business owners have to get their bookkeeper to work out for them. Most bookkeepers work this out in Excel based on the depreciation rates provided by the ATO. However, if you have already created a financial forecast in Excel, you won’t need to get your bookkeeper to do this for you.

Individuals can claim depreciation too

Even if you’re not a business owner, but you’ve still built a granny flat that you intend to rent out, you can claim depreciation in your tax returns. Instead of entering the depreciation into Xero, you’d include it on your annual tax return, so it’s really important that you work this out in Excel first and regularly update it.

***

Once you know how to use Excel for financial forecasting, you can use the same formulas and modelling for any financial forecast — be it for a granny flat project, business investment, anything that requires you to make a financial decision. Visit our website for more information on our advanced Microsoft Excel Training Course, with its new granny flats case study.

Do you want to brush up your Xero skills? Or perhaps you use MYOB but want to get a handle on Xero? Check out our suite of Xero training courses — all available for one low price.

Type the first 3 characters to discover courses, up-skilling programs and CPD articles.

EzyLearn's Career Academy

Enrolled into an EzyLearn course since 2013? Get access to new & updated course content and support by joining the EzyLearn Course Refresher Access membership Program. See how to extend your course life & support.

Xero is a great bookkeeping program for tradies who are on the go and using their phones (or a tablet) all the time. From receipts scanning to creating quotes and invoices, receiving payments and keeping track of project costs.

bookkeepercourse.com.au/produ…

Online delivery of this content allows your staff to complete the course at their own pace, in an informal environment — at home or at their desk at work, rather than in a dedicated training centre on a dedicated day — and it also allows you to monitor their progress.

Online delivery of this content allows your staff to complete the course at their own pace, in an informal environment — at home or at their desk at work, rather than in a dedicated training centre on a dedicated day — and it also allows you to monitor their progress. At EzyLearn you can choose from

At EzyLearn you can choose from

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

Magazine or journal subscriptions, domain name registrations, business name registrations, car registrations, website fees, insurances — collectively they add up, but they’re also the easiest to forget.

We recently updated our advanced

We recently updated our advanced

{kind=link}