WHETHER YOU USE A contract or remote bookkeeper, it’s crucial that they keep your bookkeeping in good order. If you ever have to replace them, you don’t want to be redoing your entire bookkeeping system.

So what are some ways that bookkeepers can work, and what can they include in their bookkeeping, that makes it easier for someone new to pick up the reigns? Let’s take a look:

The sales spiels of many of the notable online accounting software packages like QuickBooks, Wave Accounting, Outright, Kashoo, LessAccounting, Clearbooks and even Xero, claim that this feature will save you time and effort as it imports your bank transactions. The truth is, this is not foolproof and won’t work 100 percent of the time (even if it’s just a matter of not being able to get your software and your bank to “connect” just as your mobile phone connection inexplicably doesn’t work sometimes).

Therefore, always double check your bank transaction data has been imported accurately. This said, importing your bank statement into Xero (or whatever accounting software you use) is a really important step in the bookkeeping process that a lot of business owners forget or don’t know how to do. And the technology is only going to get better!

Using the correct format

To import your bank statement into Xero, you must ensure it’s in the correct format. Xero can only work with a CSV file of your bank statement. Depending on your bank, you might be able to download your bank statement as a CSV file from your internet banking, or you will have to create one from scratch.

Creating one from scratch isn’t too difficult. If your bank doesn’t give you the option of downloading a bank statement as a CSV file, you can create one yourself in Microsoft Excel.

You can download an Excel template from Xero. It includes the recommended fields and is already set up as a CSV file, so all you need to do is add in your data.

Set transaction rules

Once you’ve created and uploaded your bank statement to Xero, you’ll need to set up transaction rules for recurring expenses. You’ll learn how to do this in our Cash Flow Reporting, Budgets and ROI Xero Course.

Setting rules for recurring transactions helps speed up the reconciliation process, which depending on the type of business you operate and how often you reconcile your account, can be the most time-consuming part of the process.

Importing your bank statement and creating rules for transactions that occur each week, month fortnight, year, etc, greatly speeds up this process.

No CSV? Use bank feeds

If your business has lots of expenses every week, and your bank doesn’t let you download your bank statement in a CSV format, you may find that manually creating one in Excel each month is too time consuming.

Set up bank feeds instead. Bank feeds is the process of linking all of your business accounts, whether they’re credit cards or bank accounts, to your accounting software, so that each time you make an electronic purchase, it’s automatically imported into your accounting software.

This will allow you to reconcile your account each fortnight, week or more frequently, if you desire, than once a month when your bank statement comes in.

Learn Microsoft Excel from scratch or brush up your Excel skills, at your own pace, with our affordable Excel online training courses — where you get THE LOT (that’s 9 courses in total) for ONE LOW PRICE — everything included! Volume corporate discounts are available and our courses count towards CPD Points. NOW is the time to learn to use Excel, one of the most-used software applications in the world.

A bookkeeper who’s certified in a particular accounting software may not mean that much for your business. Better to have someone who is simply a good bookkeeper. Period.

Now that virtual bookkeepers have become more common, lots of business owners have started selecting bookkeepers based on their affiliation with an accounting application. Such bookkeepers are often called a Certified Advisor (Xero), Pro Advisor (QuickBooks) or Certified Consultant (MYOB). But are they really the best bookkeeper for your business?

What are Certified Advisors, Consultants and Pro Advisors?

In a nutshell, a certified advisor, consultant or pro advisor is just an individual who has been endorsed by a software company because they’ve demonstrated a high level of knowledge and skill with a particular accounting product.

Hiring a bookkeeper who’s been endorsed by MYOB, say, means you shouldn’t have to worry about whether your bookkeeper has set up your accounting package correctly, or whether they’re using the correct codes. What it doesn’t guarantee, however, is that each consultant or advisor is a highly experienced BAS agent, as the certification relates to their software knowledge only.

Certified Advisors and Pro Advisors go through their certificate, which is often free, because it elevates their own profile. It can also demonstrate that they are committed to that software program more than others. The Xero Certification training (at the time of writing) has a strong focus on understanding how to use the Xero Agent portal to bring clients onto the platform – and not so much about learning bookkeeping or to become a BAS Agent.

If you don’t have an accountant or BAS Agent then you should make that your starting point as everyone needs someone who can perform tasks that relate to tax and GST who acts on your behalf. If you have that setup already you can hire someone who has good bookkeeping skills using MYOB or Xero but is cheaper because they are not registered or licensed. This junior bookkeeper can perform your office admin, accounts and even customer service while your Registered BAS Agent or Tax Accountant can sign off on your financial figures.

Find a highly qualified BAS or tax agent instead

Sure, a bookkeeper who’s experienced in your accounting package is important. It’ll help keep your bookkeeping bill down because they’re able to perform certain functions quickly, while your accountant shouldn’t need to fix any errors, either. But that’s only providing that they’re as knowledgeable in Australian tax as they are MYOB or Xero or QuickBooks.

Unfortunately, however, the two aren’t mutually exclusive. So instead of focussing on a bookkeeper’s software experience, it’s more beneficial to ensure they’re qualified BAS and tax agents, with either a Certificate IV in Bookkeeping or higher.

If you don’t get a bad reference from their current and former clients, then there’s a pretty good chance they’re proficient in the major accounting packages, and if they’re not, most bookkeepers will tell you upfront.

Get the accounting package that’s best for your business, not your bookkeeper

There are lots of reasons a bookkeeper would choose to become certified with a software company, the biggest being that they get their accounting software for free and receive a commission for each new client they sign up to use the accounting package they’ve been certified with.

However, when you hire an independent bookkeeper who’s well-versed in a few different accounting packages, you’re more likely to get better advice about which accounting package is best suited to you and your business’s needs, rather than the accounting package that will generate income for your bookkeeper.

***

Are you looking to brush up your skills in cloud-accounting packages like XERO, MYOB or Quickbooks? We provide a range of online training courses in all of these packages at ONE LOW COST for ALL SKILLS LEVELS. Find out more.

We feature our own online directory of local bookkeepers looking to add to their customers. Visit National Bookkeeping to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

Help us help you get your business financials set up right

Taking time to set up your accounts correctly at the outset and recording your reconciliations regularly will save you time, money and a nasty, aching headache!

SO WE’RE INTO THE new Australian financial year. With the start of each financial year comes the chance to right last year’s financial habits and avoid repeating them again. You know what they say about people who repeat the same actions over and over again expecting different results …

If you had a crazy end of financial year, try starting off the next 12 months (well, 11 now, can you believe it!) on a positive footing, with these good financial habits.

Check your accounting software is set up correctly

Something that causes businesses and their owners countless headaches at tax time is accounting software that’s been setup incorrectly or not set up completely. Transactions that are coded wrong or bank feeds that are connected to the wrong account — or too few accounts — can leave you in the middle of a bookkeeping nightmare come June 30.

Spend some time sorting this out, or employ a bookkeeper to get you set up correctly. It’s worth that little bit of extra time now to get it right, truly!

Aim for daily reconciliations

Reconciling your business accounts regularly is important for a number of reasons, fostering good habits being chief among them. You may not need to reconcile your accounts each day, but it’s certainly a lot easier to find 10 or 15 minutes two or three times a week, rather than two or three hours once a month. The most often you do your bookkeeper the more unlikely it is that you’ll leave it pile up, eventually requiring costly rescue bookkeeping. You’ll also have a much better picture of your business’s performance with current accounting data.

Monitor cash flow

Positive cash flow is the marker of a healthy business. Negative cash flow is not. There are plenty of seemingly profitable businesses suffering negative cash flow that threatens to put them out of business. Don’t let yours be one of them. Create your own cash flow forecast reports in Excel or use a cash flow forecasting or expense app to determine if you’ll have enough money in the bank to meet your ongoing commitments (which includes paying yourself a living wage to meet your personal commitments).

That’s not to say there are no expense apps that integrate with MYOB. There are. Receipt Bank is one, Squirrel Street is another, and there are probably a lot more on the MYOB marketplace (or add-ons page). Probably the best expense tracking application we found is ExpenseManager, and it only integrates with MYOB.

And while it’s a great expense app for professional services businesses or tradespeople, Expensify is also great for retail and online shops or hospitality businesses.

Take a photo of bills and invoices from suppliers and upload them to Expensify, which will input all of the data and then send it through to Xero.

Create expense reports

Online and offline retailers don’t have to worry about this too much unless they also produce their own products, but for cafes and restaurants that host functions or cater for events, separating the expenses directly related to those functions and events is an important way to track their profitability.

Automatic approvals cut bookkeeping time

By turning on the automatic approvals feature and setting expense rules, you can cut your bookkeeping time by having recurring or trivial expenses automatically approved and sent to Xero, so you can spend more time on the complicated ones that require closer inspection.

By keeping an eagle eye on your expenses using Xero and Expensify you’ll be able to see precisely where your business is most profitable and where it’s not so you can modify it accordingly.

***

Our Xero training courses will show you have to track expenses in Xero and how to connect third party apps to your Xero account. We offer ALL SKILLS LEVELS for ONE LOW PRICE. Find out more.

Are you in business as a bookkeeper, tradesperson, retailer, trainer or real estate agent and want to stand out from the crowd? We can teach you the online marketing techniques to help you do just this! Check out what’s included in our comprehensive Social Media and Digital Marketing online training courses.

There’s more to profit and loss than meets the eye: Sometimes a company’s losses outweigh its revenue, but it doesn’t mean that company is in a bad position.

It’s not the most detailed financial report, probably because the company itself is still in its early stages — there’s actually a good argument against early stage ventures listing on the stock exchange, but that’s fodder for another post.

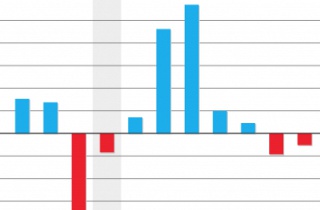

Revenue vs. losses for the period

The good news for BuyMyPlace is that its revenue increased 129 percent on the prior comparative period (PCP) to $1 million for H1 FY16/17, up from $133,518 in H1 FY15/16.

That’s an impressive leap in revenues in just 12 months, however, the BuyMyPlace financial results also reveal that the business made an even greater loss of $1.7 million, an increase of 1205 percent on the PCP.

A closer look at the report shows that, while the losses increased more than a thousand percent, it was due to an increased investment in marketing and advertising — principally on TV spots which totalled $517,723 compared with $98,578 the year prior.

This resulted in an 80 percent increase in the number of listings on the site (that is, the number of people using BuyMyPlace to sell their home), while order value increased 27 percent (people who were choosing more expensive packages).

BuyMyPlace is in good health

Although this business recorded losses that outweighed its revenue, BuyMyPlace is still in good financial health.

The report also shows that it has over $4 million in cash and cash equivalents, and only a little over $600,000 in liabilities. Although the liabilities have increased, it’s not due to taking on any additional debt — indeed, BuyMyPlace has paid down all of its loans — but was instead due to a 786 percent increase in staff salaries and, as a consequence, an increase in staff provisions and benefits — i.e., sick and annual leave.

Strategy for future growth

Not many homeowners actually want to sell their properties themselves — one estimate puts it at around 7 percent of the total number of homeowners. However, most people do want greater clarity around how the process works (including fees and commissions) — even if they still want assistance selling their homes.

Perhaps realising this, or perhaps in response to increased competition in the fixed-fee real estate services (see: Purplebricks, Settl, etc), BuyMyPlace also launched its own full service package, giving homeowners access to a real estate agent to sell their home for a fixed fee.

This will enable BuyMyPlace to capture a greater volume of homeowners, who are looking for a low cost alternative to sell their homes, but who don’t want to do it entirely themselves.

The other strategy for growth: increasing listing depth revenues.

At some point, BuyMyPlace will stop growing its market share. Or, in other words, the market of people looking for a low-cost option to sell their home will be tapped out.

But as a business, and as a publicly listed one, BuyMyPlace will need to keep growing its revenue, not merely keep it steady. It’ll need to do as other real estate services, such as REA Group and Domain have done, and increase listing revenue depths, by selling more expensive packages to customers.

BuyMyPlace will need to find additional value it can sell to customers, without necessarily increasing its own expenses to do so — or putting up its prices, which a business can usually only do once it’s cornered about 65 percent of the market, and BuyMyPlace is a long way off that yet.

***

That’s a lesson for every business owner out there. And it’s something we cover in our online Business StartUp Course.

You’ll learn how to run and understand the financial reports for your business in our Xero and MYOB training courses. You can also learn about strategies for business growth in our Business StartUp Course. Or for more information, visit our website.

The simple act of creating an Excel spreadsheet to itemise your expenses can help you keep track of everything eating into your business’ cashflow – even if not strictly deductible.

HAVE YOU RECENTLY STARTED running your own business? Whether you have, or whether you’re about to, reconciling your bank accounts regularly is probably one of the best ways to monitor your expenditure in relation to your income.

Your accounting software will help you to keep track of your income and business expenses and other important things that will affect your start up — such as how long it takes to get paid — while an Excel spending or expense sheet will help you to monitor all of your spending, business or otherwise.

The bank reconciliation process

This starts when you get your bank statement, but you can speed the process up, by entering recurring expenses into your Excel spreadsheet as they occur.

In your Excel spending sheet, you’ll enter the expense in total, but in your accounting software, you’ll only enter the percentage of the expense that relates to your business.

Identify cash flow problems

If your business has poor cash flow, using an Excel spending sheet in addition to your accounting software will allow you to identify what’s causing your cash flow problems. Sometimes cash flow problems are caused by later payers, due to poor credit management processes. Other times, however, you may find that you’re simply not earning enough to cover your expenses each week or month.

To remedy this immediately, you should look through your Excel spending sheet and see if there are any expenses, either business or discretionary ones, that you can reduce or eliminate. Then you should work on increasing your income. That’s easier said than done, which is why you should reduce your spending first.

Forecasting profit

If you don’t identify any cash flow issues, you will be able to begin forecasting profit. Typically, profit just refers to the income left over after all your business expenses have been accounted for.

But there are plenty of start ups and sole traders, who have a profitable business but are not profitable themselves.

That’s because there are many other expenses in your ordinary life — the remaining 70 percent of your internet bill, for example — that you still need to pay for.

If you’re also recording all your other expenses in an Excel spending sheet, you’ll be able to forecast your business’s profit, as well as your own personal profit (otherwise known as savings) with much greater accuracy.

The chart of accounts

In effect, what you’re doing here is creating a chart of accounts. You’ll learn more about the chart of accounts in our Xero and MYOB courses, but they are, in a nutshell, a financial record of every account — asset, liability, equity, revenue, etc — in your business.

We feel your pain! Often businesses lack the cash flow to make super payments, but you always have to pay them in the end…

WHEN YOU’RE SELF EMPLOYED you are responsible for managing your taxes and your superannuation — the latter of which many business owners let go by the wayside. It’s almost always because they don’t have the cash reserves to contribute to their super fund regularly enough.

Just as you would create a budget to make a business investment or asset purchase, you can use Xero and Excel to determine how much super you should contribute on your behalf, and then make the payments.

Run a cashflow report

You’ll learn how to run a cashflow report in our Xero training courses. This report will show you the periods when cashflow is liquid and when it isn’t. Run a cashflow report for a couple of different periods, and export them into Excel. This will give you a better idea of trends and cycles in your business.

You can also use a cashflow report to determine your income before taxes, expenses, and so forth. Superannuation is determined based on gross earnings — or revenue — so you should use this figure to work out your super contributions. This is especially important before end of financial year!

Determine super contributions

At time of writing, the superannuation guarantee is 9.5 percent of your gross revenue, before taxes, expenses, etc. If you set your prices correctly, you should have already factored this 9.5 percent into your prices or hourly rate. If you haven’t, you ought to consider revising what you charge customers and clients.

If you were an employee of a business, your employer would be required to make super contributions on your behalf, at least each quarter. Because you’re self-employed and self-managing your super contributions, you can make them as frequently or infrequently as you like, so long as you’re contributing the correct amounts. (Speak to your accountant or financial advisor, however, if you’re salary sacrificing above the minimum amount — this may affect your tax.)

Make super contributions

Once you’ve determined how much you should contribute to your super fund each quarter, refer back to your cashflow report and to the periods where your cashflow is especially liquid. Are you able to make your contributions each quarter easily, and without compromising your business’s liquidity? Would it be easier to make smaller, more regular contributions?

The decision is yours.

Use Xero to make your super contributions. Xero is connected to a superannuation clearing house, and if you’ve been using to Xero to pay yourself a wage, it’s the easiest way to do so. If you’re not using your accounting software to pay yourself a wage, you can make the payment directly out of your bank account, however, you’ll need to track this in Xero for taxation purposes.

***

Our Xero training courses will show you how run cashflow reports and make wage and super payments, while our Excel training courses will also teach you how to create business budgets and forecasts. Visit our website for more information.

If you thought you’d never have to write another resume as a contractor or self-employed business person, then think again.

STARTING YOUR OWN BUSINESS does not mean you’ll never need to write a resume or cover letter again. We’ve written about this topic before — indeed, when you first start your own business you’ll probably spend a lot of your time applying to work with other businesses directly or through a recruiter.

And the truth about being a freelancer or contractor is that you’ll most likely spend the rest of your working life applying for work. If you don’t like the idea of this, well then maybe being self-employed isn’t for you! Why? Because in order to find the best work; the kind that you’ll love, you need to be always looking for it — or always be closing, if there any fans of Glengarry Glen Ross in the house tonight.

The truth about being a freelancer or contractor is that you’ll most likely spend the rest of your working life applying for work.

Do pay attention to design

I’m choosing to exclude the “grammar, spelling and punctuation” portion of this list, because if you don’t already know that’s important by now, then oh boy, I can’t help you. But formatting and design are important, whether you’re looking for work in a creative industry or not.

The key is to grab attention in less than half a minute. You can use different fonts, for instance, a larger plain font for headings and a smaller (perhaps serif) font for the body text. You can type your resume up in Word or use PowerPoint or some other design tool. But just don’t get ahead of yourself and use something too fancy that you don’t have a proper grasp of and end up with a resume that is hotchpotch and messy.

These days, some recruiters will even upload your resume into their own “system” which “parses” your content and basically re-formats it all into plain text. If this happens, your gorgeous CV will look very different on the screen of the employer. The simpler the design and layout of the original resume, the easier it will be for them to read if they indeed use this system for getting through the applications of hundreds of job applicants. But don’t feel disheartened, there are others ways to get spotted amongst the crowd.

Don’t use jargon

The next hurdle, once you’ve got the recruiter or hiring manager reading your resume or cover letter, is to urge them to call you. Do not, I repeat, do not use jargon of any kind in either your resume or cover letter. The minute someone reads a sentence that starts with or contains “experienced in”, “team player”, “responsible for”, etc, etc, they switch off.

These phrases mean literally nothing. Nothing. Telling someone you’re a team player: redundant. Everyone should be a team player, and there is no one, not a single person ever, who has written on their resume that they’re not one. Instead, tell the employer what you like about working in a team. (On a similar note, also avoid the term “able to work autonomously” by explaining the times you’ve had to and how that’s gone.)

When you go to use the words “experienced in” try to remind yourself that this is something that happens to you — not something you proactively go out and do. Instead refer to your background in terms of achievements. Search “typical jargon to avoid on a resume” for more.

Do show your personality

Remember that employers are people too. Work culture is important to lots of businesses, so they need to know that any potential new hire, freelance or otherwise, will be able to fit in and work with them. And if you can make the person reading your resume laugh, oftentimes you’ll get a call back.

Don’t list silly interests

I should add a qualifier to that, which says that it’s okay to list a really silly interest if you know and make a point of noting that it’s a silly interest. This makes you seem thoughtful, and definitely not as dumb as a person who says they like reading or sports on their resume. Reading what? It implies novels, but it could also mean signposts, Aldi catalogues, Post It Notes. And if you like playing cricket more than once a year on Boxing Day, then for the love of all that is holy (cricket on Boxing Day), say that. Otherwise, put down interests that you actually are interested in — they reveal a lot about the type of person you are, which again, goes to help with the point above.

We mentioned that Jerry should use his accounting software to determine whether his he’ll have the start-up capital required to fund his new venture for the next 12 months. The best way to do this is to create a cash flow forecast, and we’re going to show you how.

Cash flow is a better indicator of available funds

If you’re wondering why you wouldn’t create a profit forecast, it’s pretty simple. Cash flow represents money in the bank, after you’ve paid all your suppliers and staff and loan repayments and so forth, while profit just shows how much the business earned but doesn’t take into account any cash outlays.

Profit just shows how much the business earned but doesn’t take into account any cash outlays.

It’s important to understand that it’s not uncommon for businesses to be profitable; however due to cash outlays, these same businesses may not actually have enough money in the bank to fund investment, or in this case, a new venture.

Generating a cash flow report in Xero

Follow these steps in Xero to generate a cash flow report for your business:

Go to Reports, then click All Reports.

Under Financial, select Cash Summary.

Enter the following report settings:

Date — The latest finalised month

Period — 1 month

Compare With — Previous 11 Periods

Select the Include GST and Show YTD filters

Click Update to generate the report in Xero

At the bottom of the report, click Export and select Excel to download the report in Microsoft Excel format.

The messy startup needs Xero Cashflow Training

There is a great business case study with lots of practical exercises in the Xero Cashflow Training Course. You’ll learn how to code and manage lots of different types of transactions and reconcile 2 quarters worth of transactions and end up producing cash flow reports to make financial sense of it all.

You’ll even be able to highlight alternative ways of financing some of those transactions.

Set up formulas to forecast 12 months ahead

In Excel, you’ll need to create formulas that will show you the average cashflow of your business across the previous 12 month period, so you can then forecast ahead for the next 12 months.

If you don’t use Xero and you’re using MYOB or QuickBooks, our MYOB and QuickBooks training courses will also show you how to run cashflow reports, among many others.

Xero’s reports can help you decide to buy or rent your business premises

There are pros and cons to owning your business premises depending on your circumstances, but appreciation is a significant benefit.

A BIG DECISION FOR A NUMBER of business owners is whether they should buy their own premises. And because there are upsides and downsides to both owning and renting your business’s premises, we’re going to look at some of the considerations you should take into account first.

Buying is an appreciating asset

The biggest advantage to buying is that it’s an asset that appreciates over time. As such, purchasing a property can provide your business with an additional source of income that, over time, will allow you to grow your business.

Buying also gives you access to equity that will allow you to use the property as a guarantee when you’re striking deals with potential suppliers and clients.

That said, you shouldn’t overlook the upfront costs associated with buying. In particular, you’ll need to ensure you have the appropriate amount of capital available before you can buy.

Our online Xero training courses show you how to run reports that will help you make the vital business decisions; particularly relating to how a capital outlay like buying commercial premises would likely impact your cashflow.

Renting is flexible

If your business is relatively new or it’s generally difficult to predict your future growth over the next five to ten years, renting may be a more viable option. This allows your business to remain agile and offers flexibility that buying doesn’t.

Renting, for example, offers a better range of property types of locations that mightn’t be within your price range if you were to buy.

Furthermore, shared office spaces or co-working spaces are good options for businesses with a small, mostly virtual team, or startups looking for meet like minded individuals.

You miss out on equity gains when renting

The main downside to renting your business premises is that, over time, it is your landlord’s equity you are contributing to, rather than building your own asset.

***

Using your accounting software to determine the financial health of your business will help you to make important business decisions. Our Xero training courses will teach you how to run different financial reports. Visit our website for more information.

Struggling to manage your online payroll management? Our Xero and MYOB courses will help you get the most out of this software so you can manage payroll in house.

MANY COMPANIES OUTSOURCE PAYROLL because it contains many moving parts. For instance, there’s the payment of wages each week or fortnight or month, sure. But there’s also superannuation contributions, PAYG obligations, annual and sick leave accrual.

Fortunately, most accounting apps like Xero and MYOB have made payroll easier to manage, particularly if you only have a handful of employees.

Superannuation clearing houses

Nearly every major cloud accounting package has a connected superannuation clearing house within its payroll package. Xero and MYOB are both SuperStream compliant, a government initiative to help business owners tell which accounting software apps will let them make electronic superannuation payments. And QuickBooks uses a partner payroll system which is also SuperStream compliant.

Batch wage payments

Electronic superannuation payments are one way that paying staff is made easier, but paying a dozen or so employees individually each week or fortnight can be tedious. Fortunately, both Xero and MYOB have a ‘pay run’ function that lets you make batch wage payments. This eliminates the tedium of paying employees individually, as well as the potential for error.

Accounting software calculates entitlements

MYOB, Xero and QuickBooks, if you’ve set up your employees correctly and have the appropriate payroll subscription, will also calculate your employees’ sick and annual leave entitlements, also reducing the time it takes to process payroll and the potential for error.

EzyLearn courses now include real life case studies

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our Excel Ad Hoc Payroll case study which is part of our Intermediate Excel Online Training Courses. Where possible, we draw on real-life case studies as examples, to help you learn, and apply your skills, in a relevant way that makes sense. Visit our Micro Courses page to learn more.

You Can Use the Calculation Fields in our Excel Exercises as Often as You Like!

We keep all the calculation fields in our Excel course exercises unlocked so you can play around with different figures of your own as often as you like.

DESPITE THE POPULARITY OF cloud-based accounting software applications like Xero and MYOB, Excel still remains one of the most indispensable software programs for businesses and individuals alike. That is why we always make it a priority to constantly update our Microsoft Excel Training Course.

You can apply Excel to so much

Accounting software, even robust packages like MYOB, only allow you to perform a finite number of functions that relate to business accounting. However, Excel can be used for a multitude of different purposes — both business and personal, merely one of which is to develop a financial forecast for an investment.

But even though, with the current property booms in our major cities, granny flat construction has become more common, it is not so common that every person taking our Excel courses is planning to build a granny flat for their next investment. That’s why we decided not to lock our course content.

What does this mean? It means that all the calculation fields in the exercise files of our Excel training courses are unlocked, so that your education remains unlocked too. You’re free to play around and replicate them as you need, so you can get a proper handle of how to use Excel in business or for work.

***

Visit our website for more information on our Microsoft Excel Training Course, with its new granny flats case study. We provide a range of online Excel training courses for beginners’, intermediate and advanced students.

Depending on the structure of your business, you may be legally required to include a P&L statement with your tax return or activity statements. Your tax agent will be able to advise you if your business will be required to file a P&L, which requires all of your bookkeeping to be up-to-date before you can run it.

Even if you don’t have to file one with your activity statements or tax returns, it’s still a good idea to run a P&L for your own sake. A P&L statement identifies whether your business has made a profit or loss and which accounting period these occurred.

Accounts receivable, payable

Find out who owes money to your business and to whom your business owes money. This is obviously part of the credit management process, which any good business will have in place already, but it’s a good idea to keep a steady eye on what’s coming in and what’s going out as EOFY approaches.

PAYG, superannuation

The end of each quarter brings a lot of PAYG and superannuation reporting, but EOFY brings a double whammy of activity statements tax returns and PAYG and superannuation compliance. You’ll need to run these reports so your bookkeeper can complete the payroll component of your returns.

Inventory stocktake

If you sell goods, you’ll need to complete a stocktake of your business’s inventory so that any missing stock can be written off, and to ensure you’re starting a clean slate for the new financial year.

We show you how to write off stock and inventory before the EOFY

Do you know how to make inventory adjustments? Our Xero and MYOB BAS and GST Reporting courses can show you how.

IT’S A GOOD TIME TO START looking at any slow-moving or obsolete stock that your business (or your client’s business) may be holding, as we’ve reached the end of Quarter 3 and have now started Quarter 4 for the 2016/17 financial year — which means the end of the financial year is fast approaching.

Writing off stock in MYOB or Xero is known as making an inventory adjustment, and our MYOB BAS Reporting and GST or Xero GST, Reporting and BAS training courses take you through the steps to do this. But first, you need to identify which items aren’t selling. We’ve created this case study to help you understand how.

Understanding your inventory’s performance

Every business needs to understand how their inventory is performing, and how it impacts their business. If the business owner is too busy to stay on top of this, then they should employ a bookkeeper to help.

A good example of why understanding inventory is important to a business is to look at an air conditioning company. This business makes money two ways:

Selling air conditioning units

Installing / maintaining air conditioning units

The margin on the sale of an air conditioning unit is not much, a few percent on top of the wholesale price. Where the business makes its money is in the installation or maintenance of the units it sells.

The business purchases three dozen units, of varying brands, models, price points, etcetera. It now needs to know which units are most popular with customers and why; which units aren’t popular with customers and why; whether it’s profitable for the business to continue to stock the unpopular units; or, conversely, whether it’s profitable for the business to continue stocking the popular units.

Inventory reporting

The business’s bookkeeper regularly runs a number of reports in their accounting software, including profit and loss reports and stock-on-hand reports. These reports are used to identify which units sell quickly, as well as the units that take longer to sell, and the profit margins on each.

The units that sell quickly don’t require a technician to install them. Although they’re responsible for the majority of sales, they don’t generate more revenue for the business. The units that sell slowly, do generate more revenue as they require installation and maintenance, however too many units were ordered and they’ve now been discontinued by the manufacturer. Some units have hardly sold, and, although not discontinued, have been superseded by newer models.

Stock write offs and future orders

Because the bookkeeper regularly runs these reports, s/he has been able to export them into Excel for further analysis. By the end of Q3, the bookkeeper can make suggestions to the business owner about the future of the business.

In particular, the bookkeeper suggests that the units that have been superseded are marked down to clear as much stock as possible, and cease any new orders. Likewise, the discontinued models will be marked down.

Orders for the units that replaced the discontinued models will halve the order volume. Likewise, order volumes for the top selling units will reduced. The profit margin on these units is very low and they result in no additional revenue from installation or maintenance. The profit that would be earned on the additional units is negligible, however by reducing the unit volumes, the business improves its cash flow.

Act NOW for EOFY

If your business sells stock or a combination of stock and services, like the air conditioning business does above, start looking at your inventory now. Markdown any slow-moving stock at the end of Q3, to give your business time to move the remainder of it. If it doesn’t sell, write it off at EOFY.

We feature our own online directory of local bookkeepers looking to add to their customers. Visit National Bookkeeping to find a suitable and experienced person available to work in your area, or able to work anywhere in the cloud. Alternatively, if you are a bookkeeper looking to expand your client list or find contract work, you can register and become part of our network for free.

Search this site

Type the first 3 characters to discover courses, up-skilling programs and CPD articles.

EzyLearn's Career Academy

Enrolled into an EzyLearn course since 2013? Get access to new & updated course content and support by joining the EzyLearn Course Refresher Access membership Program. See how to extend your course life & support.

Xero is a great bookkeeping program for tradies who are on the go and using their phones (or a tablet) all the time. From receipts scanning to creating quotes and invoices, receiving payments and keeping track of project costs.

bookkeepercourse.com.au/produ…

EzyLearn Excel, MYOB and Xero online training courses count towards

EzyLearn Excel, MYOB and Xero online training courses count towards

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our

At EzyLearn we are constantly refreshing the content of our online training courses. Relevant to those of you doing Payroll, might be our